If there is one constant in Eastern Europe, it is the lack of constancy. Nowhere else are there such frequent changes of government or desperate attempts to form a functioning government through one snap election after another. Bulgaria, for instance, had gone through a striking series of snap elections before the vote two weeks ago at least offered hope of forming a government capable of governing. The most recent case is Romania, where a first government formed last summer had already collapsed again at the start of this year and the Prime Minister is set to be ousted.

Economic problems are usually at the forefront when governments fail. In Romania, there was recently no agreement on where cuts should be made in the public sector. In Hungary too, as I recently pointed out, the Orban government faced virtually insurmountable economic problems before it was voted out of office. It is highly unlikely that the new government will find a solution here. Even Poland, where growth figures actually indicate satisfactory economic development, is part of this complex situation that is not easy to understand.

Labour costs are rising too sharply in Eastern Europe

Whether with or without its own currency: it is evidently incredibly difficult in Eastern and Central Europe to avoid a real appreciation (of the national currency or the euro). Real appreciation is nothing other than a loss of competitiveness, because domestic inflation rates, driven by very high wage increases, are rising faster than in the rest of Europe (Friederike Spiecker, Constantin Heidegger and I have already made this a key focus in the Atlas for the World Economy 2022/2023 and pointed out the looming crisis scenario in no uncertain terms)

In some cases, as I have also mentioned on several occasions, it is only wages that rise, whilst prices adjust to developments in the rest of Europe due to intense competitive pressure. But even this means that companies in the affected countries suffer reduced profits or losses, which severely restrict their ability to invest.

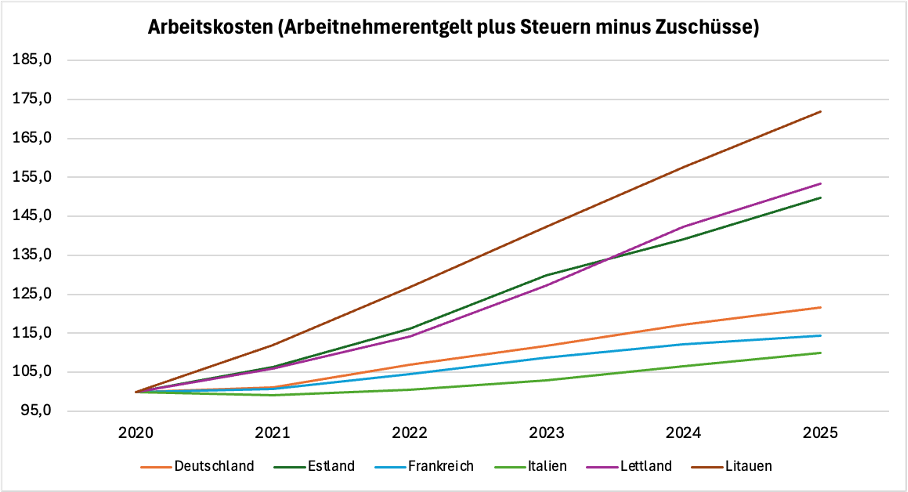

Let us therefore examine labour cost trends over the past five years in a number of countries, comparing each with Germany, France and Italy (the labour cost index can be found here on Eurostat). The trend is illustrated here using an index with a base of 2020 = 100, as the most recent specific wage developments are primarily observable in the wake of the price surge that began following the COVID-19 shock. Figure 1 shows the Baltic countries, all of which are members of the eurozone.

As was the case before the major global financial crisis at the start of the century, wage trends in the three countries have become significantly decoupled from economic conditions, as productivity gains are not much greater than in the West. In the three Western countries, the index will reach values around 120 in 2025, indicating that wages have risen by a total of 20 per cent over these five years.

In contrast, the figure stands at almost 75 per cent for Lithuania and around 50 per cent for Estonia and Latvia. This represents a real appreciation of over 50 per cent compared with the Western countries.

Figure 1

Source: Eurostat; labour cost indices by NACE Rev. 2 activity – nominal value, annual data

Source: Eurostat; labour cost indices by NACE Rev. 2 activity – nominal value, annual data

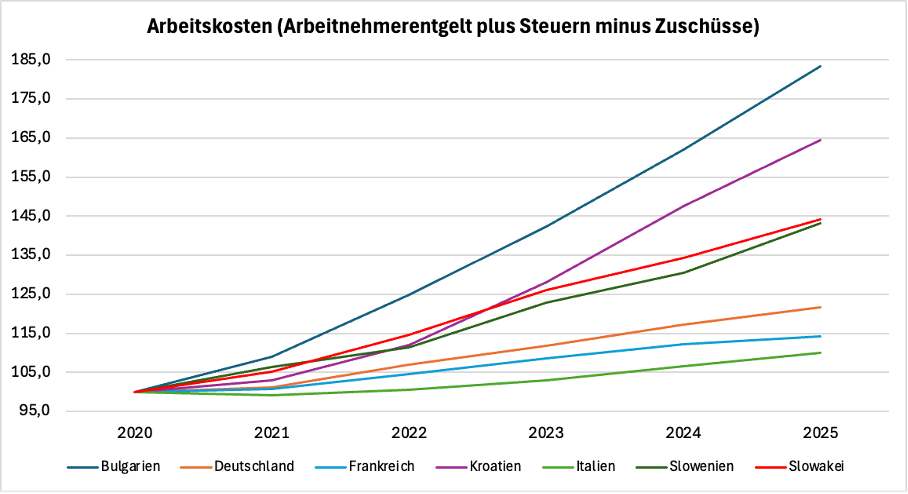

The divergence between the West and Bulgaria and Croatia is even more dramatic. Bulgaria achieves almost 85 per cent growth and Croatia 65 per cent. Croatia joined the eurozone in 2023, and Bulgaria at the start of this year.

Figure 2

Source: Eurostat; labour cost indices by NACE Rev. 2 activity – nominal value, annual data

Source: Eurostat; labour cost indices by NACE Rev. 2 activity – nominal value, annual data

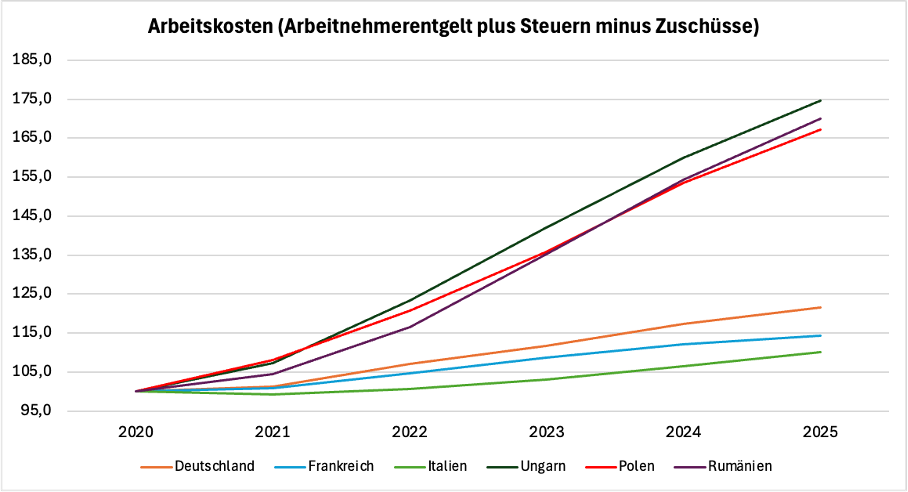

Countries that still have their own currencies are also affected (Figure 3). Poland, Romania and Hungary have seen wage growth of between 65 and 75 per cent since 2020.

Figure 3

Source: Eurostat; Labour cost indices by NACE Rev. 2 activity – nominal value, annual data

Source: Eurostat; Labour cost indices by NACE Rev. 2 activity – nominal value, annual data

These countries could free themselves from this trap if they ensured that their currencies depreciated significantly against the euro. However, this is obviously easier said than done. Devaluing one’s own currency is always difficult for governments seeking to demonstrate success. In Eastern Europe, however, this is particularly true because the euro is always immediately on the table as an alternative to their own currency. If a country’s currency depreciates, calls for entry into the eurozone automatically grow louder. Consequently, even those countries that urgently need a devaluation due to domestic wage trends try to keep their currencies stable against the euro.

The consequences will be dramatic

Any country that experiences such a significant real appreciation will, without a doubt, lose a great deal of market share and jobs to countries that devalue. The immediate consequence is usually a large trade and current account deficit, leading to these countries, like Greece before them, being put through the wringer by the international capital markets.

In Eastern Europe, however, there are a number of factors that will ultimately not prevent the crisis, but which ensure that the immediate consequences appear less dramatic for some time. Firstly, there are usually a significant number of Western companies there for which these wage increases do not trigger an existential crisis, because they have very high levels of productivity. Consequently, these companies simply absorb the wage increases.

Secondly, the scale of the problem is obscured from public view by labour migration. As long as unemployment remains relatively low, the impression is that everything is moving in the right direction. The long-term problem – that indigenous companies are systematically disappearing and the foundations of the entire economy are being eroded – is simply ignored.

Added to this is the fact that the effects of the loss of competitiveness are in many cases masked by aid payments from Brussels. The trade balance is in deficit almost everywhere, but the current account balance looks much better because the subsidies from Brussels reduce the gap. In some cases, particularly in Croatia, a very positive tourism balance also masks the massive deficits in the trade balance.

None of this, however, changes the fact that the consequences will be dramatic. In a world with free movement of trade and capital, such as the European Single Market, one cannot simply ignore macroeconomic competitiveness without eventually having to pay the price.

Western companies, which are still active in large numbers in Eastern Europe because they are exploiting the wage gap (which still exists in absolute terms), will withdraw from Eastern Europe as soon as the wage gap between East and West narrows significantly. Those countries that have not by then built up their own competitive industries will face enormous problems, because aid from Brussels will not flow forever.

I would like to thank Erik Münster for his help with the statistics