It is hard to believe the sort of things being circulated about Argentina and its libertarian president. The article that Patrick Kaczmarczyk and I wrote some time ago has generated a particularly strong response. Some (such as Poschardt and Stelter, from minute 17) even believed that they no longer needed to engage with the matter if they simply discredited the medium in which this article had appeared (namely Surplus; though it has also been published on this site and in Makroskop). That is incredibly cheap.

But even in the various forums discussing the article and a follow-up piece by Patrick Kaczmarczyk in Die Zeit, one finds an incredible number of misunderstandings that could easily be cleared up if everyone would just listen. True ideologues do not want to be persuaded, but there are certainly a number of people who have a genuine interest in understanding what is going on in the country. So I am making another entirely objective attempt.

In my observation, four arguments are repeatedly put forward when it comes to President Milei’s ‘successes’:

1. Milei inherited a catastrophic economic situation (following 20 years of almost exclusively left-wing governments) and therefore cannot be held solely responsible for the state of affairs.

2. Milei has, after all, eliminated the public deficit (for example, here).

3. Milei has significantly reduced the inflation rate.

4. The IMF forecasts substantial GDP growth for Argentina in 2025 and expects a similarly high figure for 2026; surely this cannot be ignored.

Re 1: This is entirely undisputed. I am the last person to believe that left-wing governments, particularly in Latin America, pursue sensible and appropriate economic policies. The left in Latin America knows just as little about relevant economics as the conservatives. The left was often only the left because it occasionally distributed a few dollars or pesos amongst the poorer sections of the population. Venezuela under Chávez was a prime example of this: every now and then a few dollars from oil revenues for the people, but otherwise a catastrophically poor economic policy. The ‘left-wing’ Kirchners in Argentina even manipulated inflation rates to hide from the people just how badly off they were. More on that below.

Re 2: That is correct. Forcibly eliminating the government deficit may be celebrated as a political feat, but it is economic nonsense if the state is not replaced by businesses that ensure savings are turned into investment. As shown below, this is precisely not the case in Argentina.

Re 3: Milei has not reduced the inflation rate. The inflation rate is not simply in the hands of a government. As has been demonstrated time and again on this page, it is determined to a far greater extent by the institutions that shape wage negotiations than by fiscal and monetary policy.

In Argentina, wages are strictly indexed to the current inflation rate. This places a heavy burden on policymakers, as it means that whenever there is an external shock – such as a rise in oil prices – the inflation rate rises, and wages are immediately adjusted to reflect the higher inflation rate. Logically, this leads to the inflation rate rising very quickly and very sharply once such a shock has occurred. Conversely, however, the inflation rate also falls very quickly when there is a reverse shock, such as a fall in oil prices.

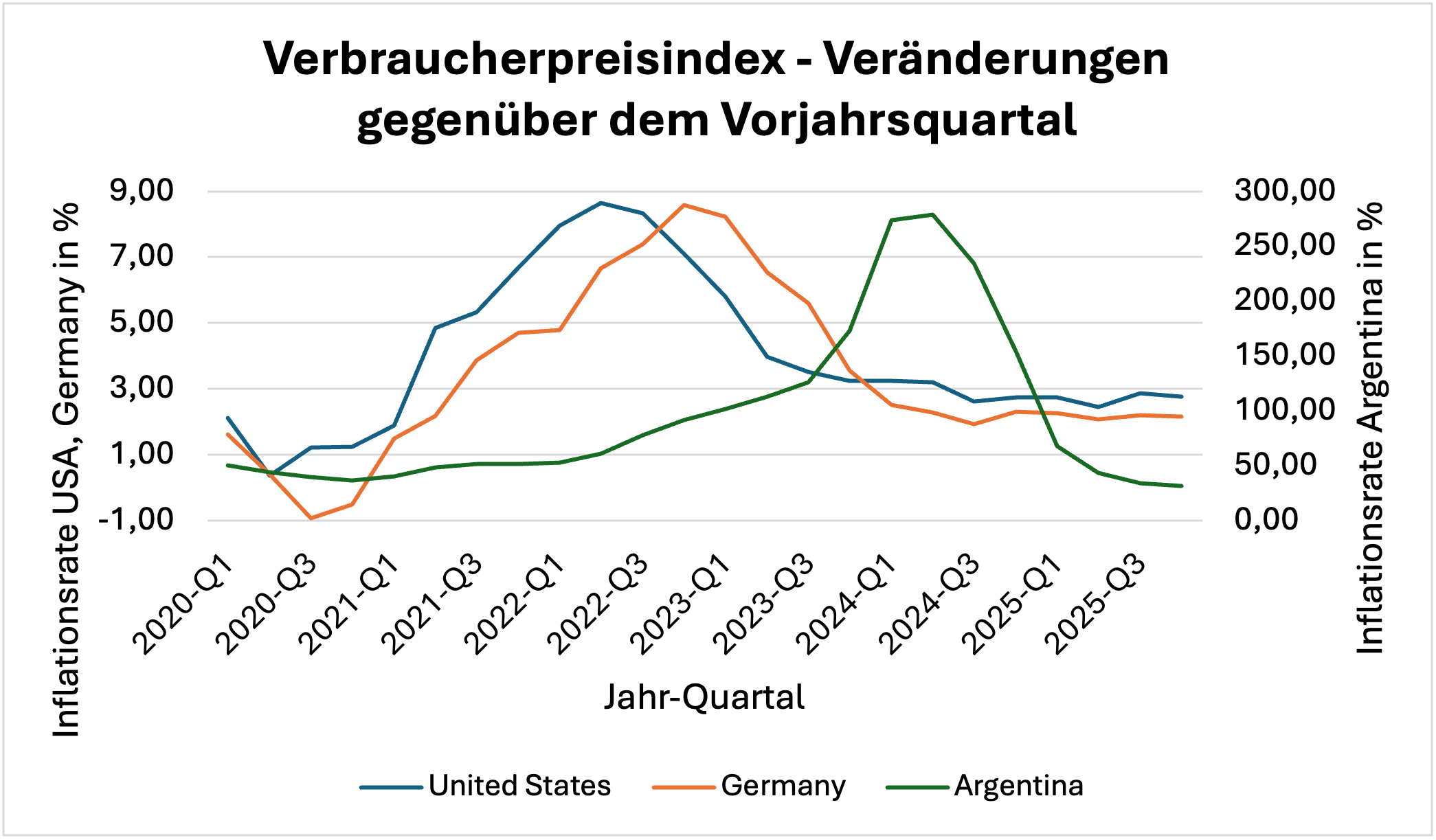

Figure 1 shows that the trajectory of the inflation rate (at a significantly higher level) is comparable to that in Germany and the US. However, it rises much faster and much higher because there is no brake in the indexation mechanism until the external shock reverses.

Figure 1

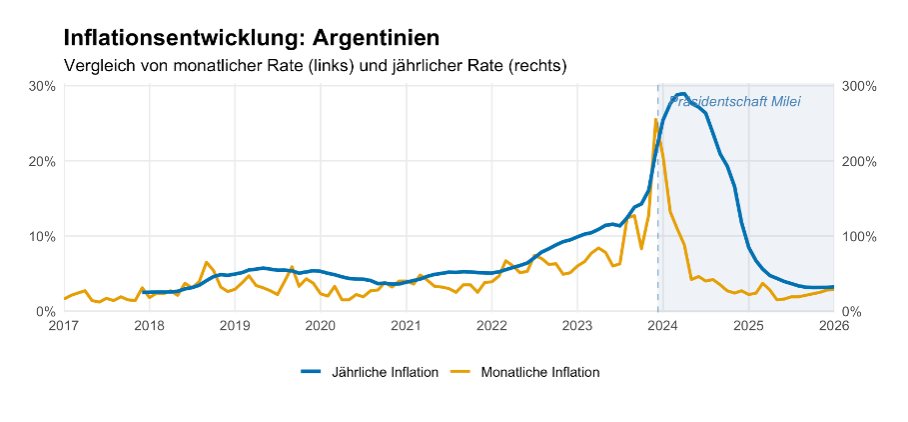

Milei came to power in October 2023, when inflation had almost peaked, as Figure 2 shows. The monthly rates, which precede the annual ones, began to fall almost exactly at the time of the presidential election (even slightly before). Milei could not possibly have influenced this.

Figure 2

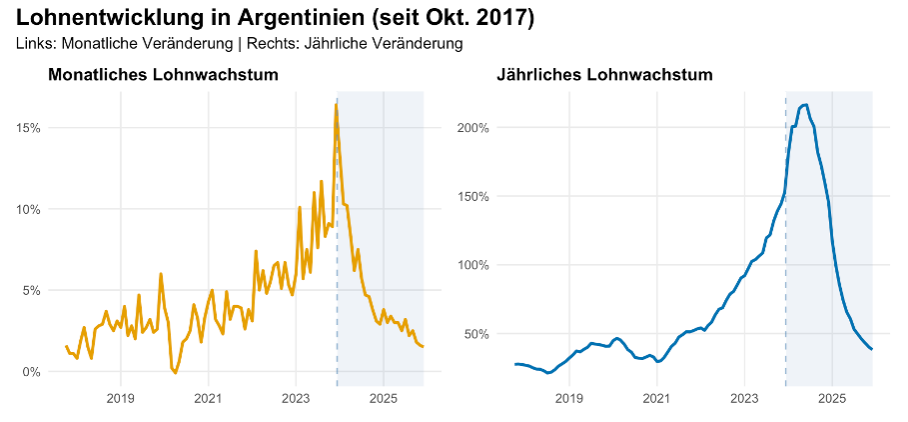

Wage trends paint exactly the same picture (figure 3). Monthly rates fall at the very same moment as the inflation rate. This is the result of strict indexation. It has absolutely nothing to do with government policy. The government has also done nothing to combat inflation; interest rates, for instance, have been consistently lowered.

Figure 3

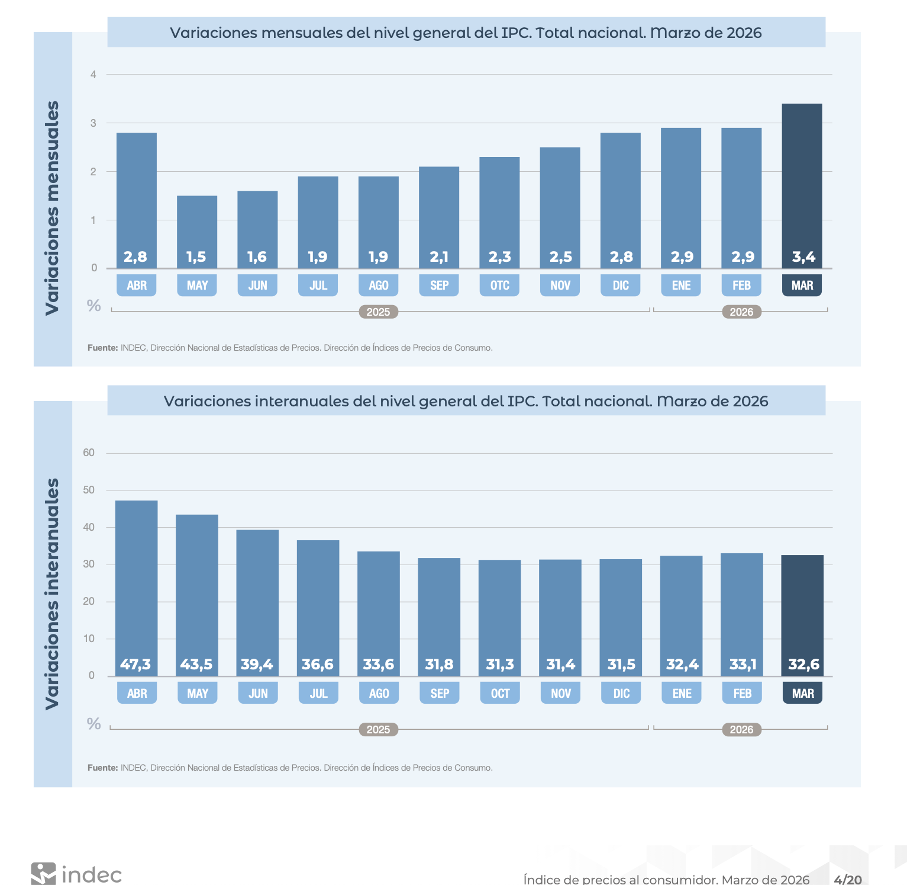

If the government is responsible for anything, it is for what happened after the crash. This brings us to the current situation. Figure 4 (original from INDEC, like all other graphs in Spanish) shows the trend in the inflation rate from April 2025 to March 2026 (monthly and annually). Since May 2025, the inflation rate has been rising slightly again, which is particularly evident – and once again far more so than in the annual rates – in the monthly rates. Last month, it stood at over 3 per cent month-on-month.

Figure 4

This is not yet a disaster by Argentine standards, but it must be a clear sign to any reasonable person that the government has so far achieved nothing in the fight against inflation and has no strategy either, as there are no signs (and no government measures) to suggest that this situation will change in the near future or next year. Should there be a further rise in oil prices this spring, the inflation rate will rise very quickly once again.

Re 4: I have a simple rule when assessing figures from statistics and values officially announced and calculated by the administration. I always trust the statistics first and mistrust all official calculations. I need only recall the German statistics scandal, which was not allowed to be one (as shown here). For three years, the Federal Statistical Office misled politicians and the public and ruled out a recession, even though the statistical indicators clearly pointed to one.

I trust the IMF even less than the German Federal Statistical Office, because it quite openly has a political agenda, particularly in the case of Argentina (as shown here).

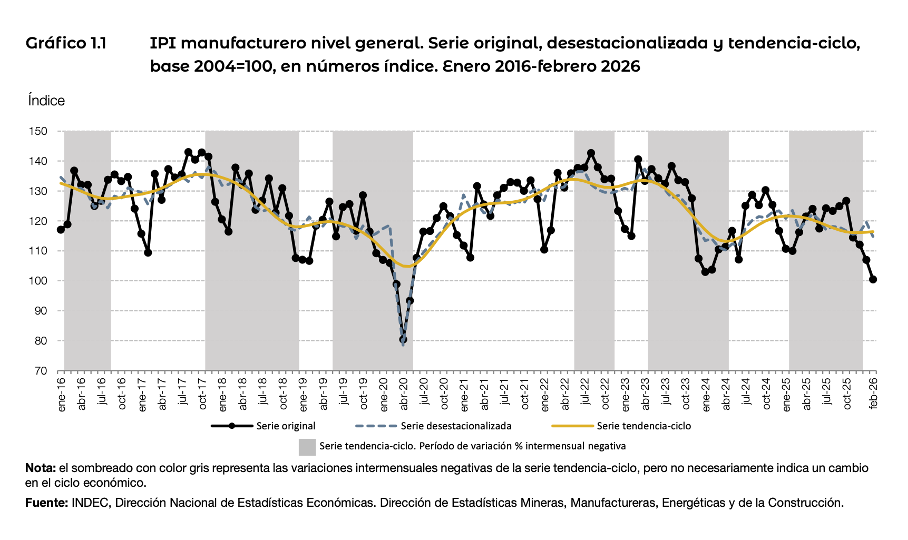

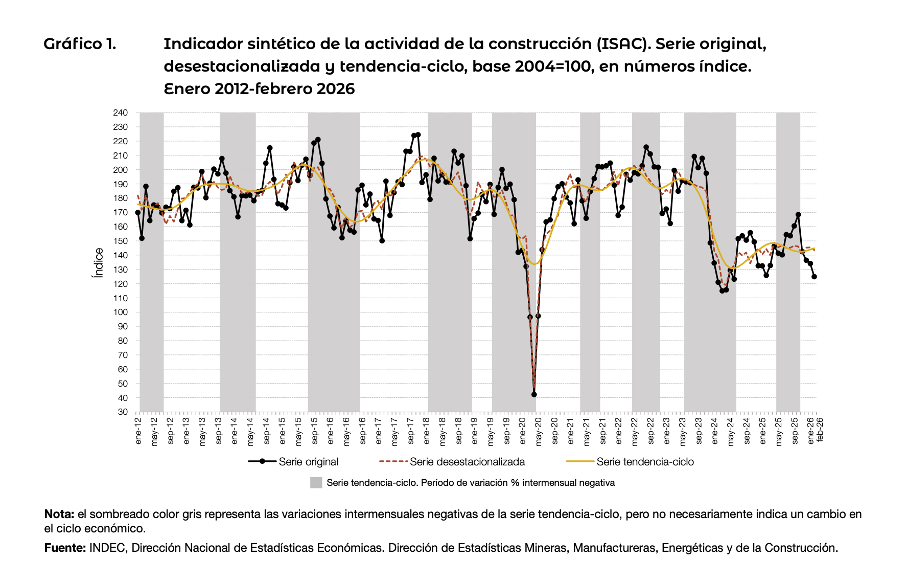

The statistical indicators, however, are unambiguous. The Argentine economy is in a severe recession in the two sectors that are particularly crucial for an economic recovery and investment activity: namely, industry and the construction sector.

In a publication dated 9 April, INDEC shows that industrial production slumped dramatically in February this year (Figure 5). The original value (the dotted line) has fallen to a value of 100, believe it or not. And this is for an index whose base value is 2004=100. This is outrageous: industrial production today is no higher than it was in 2004! This demonstrates once again that all governments since the start of the century have failed.

But it does not alter the fact that Milei has no plan whatsoever for how he intends to manage this economy better than his predecessors. Since early 2024, industrial production (seasonally adjusted, the grey curve) has been hovering at a very low level (surpassed only by the Covid shock) and there is nothing to suggest that an improvement is within reach, because there is no indicator that this economy is receiving any positive impetus from any quarter.

Figure 5

The situation is almost even worse in the construction sector (Figure 6). Although the level of production is higher here, the slump following Milei’s assumption of power was even greater. Here too, only the COVID-19 shock was worse.

Figure 6

These are simple and clear results. There may be sectors of the Argentine economy where, for whatever reason, things are going better, such as in agriculture or in the extraction and processing of raw materials. But that is not the point at issue. When a government takes office to revitalise the market economy and give the economy new momentum, it must succeed, above all, in revitalising the sectors that are the most important drivers of investment and productivity in any economy. These are industry and the construction sector.

Conclusion

If, after two and a half years, industry and the construction sector are in tatters, the inflation rate stands at over 30 per cent a year and rising, interest rates have stabilised at 30 per cent and the currency is overvalued, the government has failed spectacularly.

Imagine the furore that would raise among German conservatives if the German inflation rate were to rise to just over three per cent per annum and interest rates were to rise significantly. If, on top of that, German industry were not merely faltering but collapsing, and the construction sector were stuck at an extremely low level, they would declare any government a failure without a moment’s hesitation. However, anyone who does not even attempt to maintain their intellectual standards to some extent cannot, unfortunately, be taken seriously.