It is quite astonishing: Viktor Orbán’s heyday in Hungary began when, following the end of massive currency speculation (carry trades) that had massively overvalued the Hungarian forint, the forint plummeted and left many homeowners who had taken on debt in foreign currencies (Swiss francs or Japanese yen) due to low interest rates in enormous difficulty. Orban promised that the state would absorb a significant portion of the speculative losses – and won.

Now, 16 years later and following yesterday’s dramatic defeat for Orban, his successors face a very similar situation. Orban has steered the country into a position whose dangers he, above all, should have been aware of.

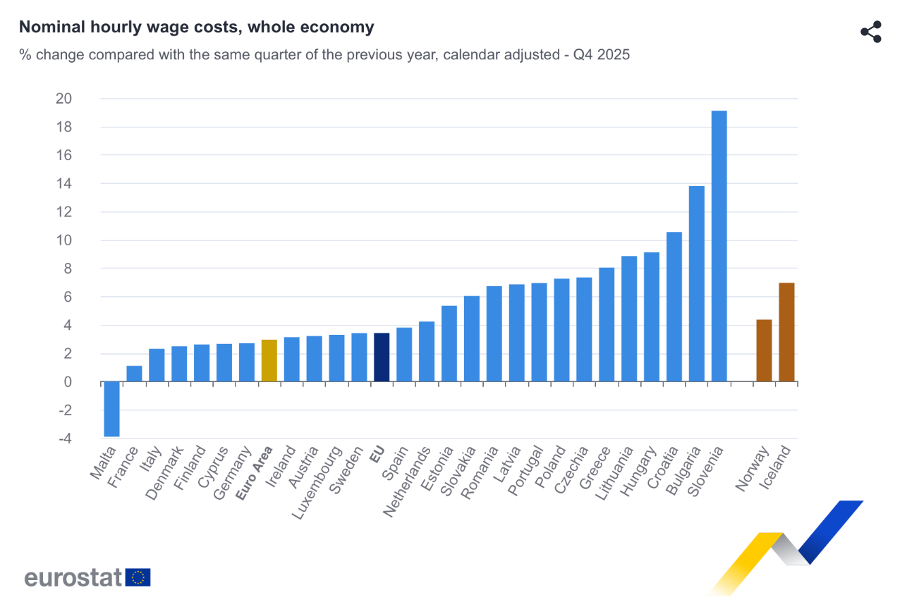

For several years now, wages in Hungary have been rising far faster than the domestic economy can cope with. The wage surge began after the price shock that followed the Covid-19 crisis and has continued right up to the present. The Eurostat chart below shows growth of over nine per cent in the final quarter of 2025. However, the highest increases were recorded between 2022 and 2024, at well over ten per cent.

This contributed to a significant rise in the general price level, particularly in 2022 and 2023. It is only since 2024 that competitive pressure on European markets has become so intense that even producers in Hungary can no longer pass on labour costs in full. Consumer prices and producer prices in the manufacturing sector in Hungary are now rising only slightly. Nevertheless, the country is still carrying an enormous burden from previous years. The producer price index, which I last presented and explained in this paper, stood at almost 150 points at the start of this year – on a par with Bulgaria – whilst the figures for the other countries are almost universally around 120. Economic development has ground to a halt over the past three years, accompanied by a sharp slump in investment.

Why is Hungary not devaluing?

This represents a massive competitiveness gap which, as I have explained on numerous occasions, is only sustainable for Western companies manufacturing in Hungary. The domestic economy, which competes with foreign markets, is being crippled in the process. Unlike Bulgaria, however, Hungary still has its own currency and could, in theory, quickly close the competitiveness gap by devaluing the forint.

But it is not that simple. In recent years, the forint has appreciated rather than depreciated. As the following graph shows, the real exchange rate of the forint calculated by the BIS has risen significantly in recent years (here, if the curve points upwards, it indicates an appreciation of the forint). This means that the devaluation of the forint, if there was one, did not offset the inflation differentials.

In nominal terms, the forint has been under repeated upward pressure since the start of 2023, as the next chart from the ECB shows (here, an upward movement of the forint indicates a devaluation). Although there was a depreciation, particularly in 2024, the forint was under upward pressure throughout 2025 and actually appreciated significantly, even though the poor competitive situation would have called for a substantial depreciation.

Where does the upward pressure on such a currency come from? Well, it is once again the famous carry trade that ultimately brought Orbán to power and which may now have sealed his fate. Because inflation rates in Hungary were significantly higher than in the rest of Europe, interest rates in Hungary have also been significantly higher than in the EMU in recent years. In mid-2023, the Hungarian National Bank even briefly raised interest rates to a staggering 17 per cent. Although they fell rapidly afterwards, short-term interest rates in Hungary still stand at over six per cent today. This represents a significant gap compared to the EMU and is therefore of interest to currency speculators. Consequently, a currency that actually needs to depreciate is being revalued.

How does one get out of this situation?

It is, however, easy to see that having one’s own currency is far from guaranteeing independence. Because the markets are driven by speculation and by no means follow the rules of traditional economics, even countries with their own currency are forced to follow a larger neighbour’s lead when it comes to inflation and wages.

Getting out of this situation is not easy, because the government and the central bank must work together to bring about a devaluation without this leading to renewed inflation (via wage adjustments). At present, with energy import prices already high, this is particularly difficult. Direct intervention in the foreign exchange market is required (buying foreign currencies with one’s own currency to weaken it) along with a significant cut in interest rates. This will only work if there is prior explicit agreement with the social partners to ensure that the interest rate cut and the devaluation are not exploited to trigger further massive wage increases, even if consumer prices rise more sharply than generally expected for a time.

As far as I can see, little is known about the election winners’ economic policy programme. Yet it is here – in the return to reasonable wage increases and the normalisation of interest rates – that the greatest challenge lies.