In the Financial Times, Martin Wolf noted a few days ago that imbalances in international trade are back on the political agenda. Although Wolf reaches entirely reasonable conclusions regarding mercantilism, he nevertheless states that it is nonsense to claim that the US trade deficits can be eliminated solely through trade or exchange rate policy. He believes that this would “also require macroeconomic adjustments, in particular a reduction in the US public budget deficit, which the IMF forecasts at 7.5 per cent of GDP for 2026”.

Consequently, Wolf lavishly praises a paper by “G7 economists” that is supposed to demonstrate what global imbalances are and how to combat them. Yet the paper (whose authors include, among others, the former Chief Economist of the IMF, Gita Gopinath, and the former President of the Bundesbank, Axel Weber) is completely misleading. Once again, the old mistake is being made (as shown here) of treating a country’s current account balance as an independent phenomenon on the basis of an identity (an ex post observation). This is regrettable. Economics has still not grasped what its actual purpose is.

The paper states:

“These relationships (the standard identities of national accounts, according to which total income consists of consumption, investment and the balance of trade, HF) show that a country’s external balance is simultaneously the following:

- a current account deficit (by assumption)

- an imbalance between savings and investment (by definition)

- a net capital flow (according to accounting terminology)”

No, that is complete nonsense; these identities do not demonstrate that at all. Anyone who argues in this way does not even know what an imbalance is. A current account deficit is not necessarily an imbalance; the ‘imbalance’ between savings and investment is meaningless because it is merely the result of an ex post identity, and what is called a ‘net capital outflow’ is likewise the result of an identity or a definition. Meaningful statements can never be derived from such a constellation of concepts and identities.

What is an imbalance in international trade?

To get to the heart of the matter, one must take a step back. There was a time when such simple relationships were taken for granted and respected in economics, but in the turmoil of the neoclassical counter-revolution and in the face of widespread model-building at universities, many simple relationships have evidently been lost.

The concept of ‘competition’ normally refers to competition between firms – both nationally and internationally. That is where the concept belongs. Firms should prove themselves in competition, and the best firm should prevail under otherwise equal conditions (which includes, first and foremost, the principle of equal pay for equal work!). Given fixed wages, a company’s efforts to improve productivity in its production processes or in the nature of the goods and services it produces are rewarded through higher profits or lower prices.

However, problems arise when countries as a whole have competitive advantages or disadvantages compared to another country. Typically, these are advantages or disadvantages that benefit all companies in one country, or disadvantage all companies. If such advantages or disadvantages exist at the national level, competition between companies in the countries involved is distorted, because even a highly competitive company may face absolute disadvantages compared to a company in another country if that country as a whole holds an advantage.

The nature of these advantages can vary greatly:

- A country may impose import duties, significantly reduce taxes for its companies, or provide high subsidies to domestic companies (Ireland).

- A country’s currency may over- or under-shoot the inflation differential with its trading partners, leading to undervaluation or overvaluation (Brazil, Hungary, Iceland and many others prior to the major financial crisis of 2008/2009). Overvaluation due to carry trade was the most common scenario at that time.

- A country’s government may opt for a system of fixed exchange rates and peg its own exchange rate to the currency of a major partner (anchoring). If the country is unable to stabilise its inflation rate (relative to the anchor country), this often leads to a real appreciation, which can only be resolved through a currency crisis (Argentina, Brazil in the 1990s, all countries affected by the Asian financial crisis).

- In a system of fixed exchange rates (or a monetary union), a country’s government can ensure that wages for all companies in the country rise less (relative to productivity) than in the countries with which it has agreed on the fixed rate. Consequently, the real depreciation creates an advantage for all companies in that country, which systematically harms companies in the partner countries (Germany at the start of the century, following the introduction of the euro).

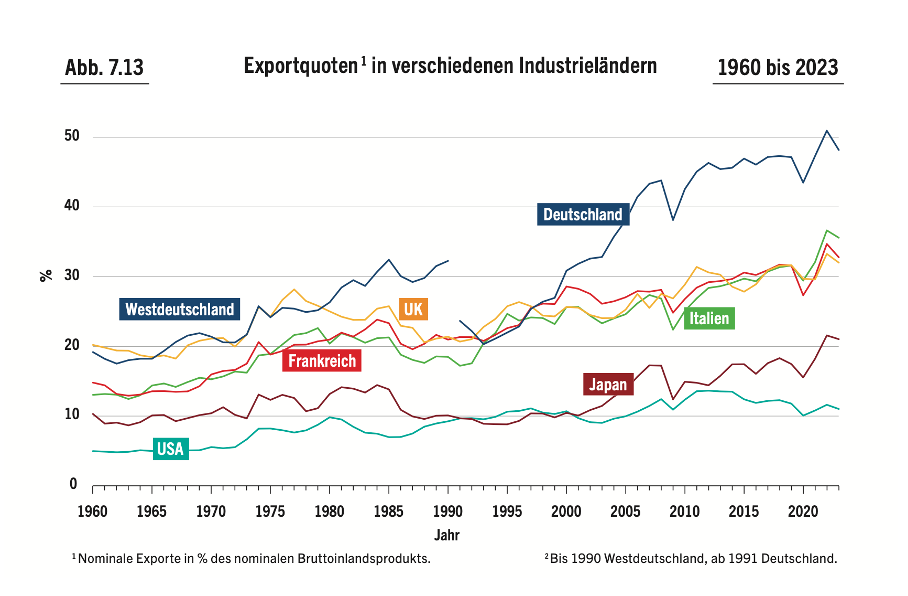

All of this has led to imbalances. It was regularly government intervention and/or mispricing on the foreign exchange markets that were responsible for the imbalance. The imbalances manifested themselves in various forms and across different indicators. Countries whose currencies have depreciated significantly in real terms typically gained market share on global markets at the expense of countries whose currencies appreciated. They strengthened their industry, saw an increase in their export share and were successful in the labour market. For example, despite China catching up, Germany recorded an enormous increase in its export share following its real depreciation, as the accompanying figure shows.

This is precisely the phenomenon that needs to be explained if one wishes to engage in serious scholarship. And the explanation is clear: through its politically supported wage dumping, Germany has devalued in real terms and consequently achieved enormous export success, which has been reflected both in this rising export ratio and in increasing market shares on the global market.

Of course, a country’s improved competitiveness also affects both the trade balance and the current account balance. But the current account balance, which is usually fixated upon, is merely one of several indicators that signal an imbalance in trade flows. This is precisely where the confusion begins. In the paper mentioned above and in many other publications, the change in the current account balance is regarded as the phenomenon to be explained; consequently, the current account balance is viewed as the imbalance itself rather than merely an indicator of the actual problem.

However, because the current account balance (in the ex post identity of the national accounts) can be written as the difference between saving and investment (see the original box from the paper), it is concluded that this identity can explain the balance. One also concludes from the fact that a current account surplus is always accompanied by an equally large capital account balance (which merely reflects the debt of the deficit country living beyond its means) that these ‘capital flows’ can play an independent role in the emergence of the imbalance.

The central equation: CA = S – I = CF, where:

- CA = current account balance

- S − I = balance of savings and investment

- CF = net capital flows

Both conclusions are incorrect.

What is referred to in accounting as a capital export is by no means a capital flow, but merely the volume of credit required by the deficit country and raised within that country to pay for the (surplus) exports of the surplus country. Not a single euro or dollar remains with which to finance anything other than the exact sum corresponding to the current account balance.

The fact that the current account balance can be described in the ex post income identity as the difference between saving and investment is irrelevant. Nor are saving and investment by any means equal ex ante in a closed economy (or an economy with a balanced trade balance). Nor is there any mechanism that would reliably ensure (the interest rate mechanism postulated by neoclassical economics certainly is not it) that saving equals investment without income having to change to bring about this balance. Even die-hard neoclassical economists should have grasped this much from the Keynesian Revolution. There is not even a theoretical mechanism for the transformation, hoped for by Martin Wolf, of a reduced US government deficit into external surpluses or falling deficits.

To put it provocatively: explaining the loss of market share that France has suffered vis-à-vis Germany in China—because it lost competitiveness—by the ‘imbalance’ between saving and investment is patently absurd. An explanation that attempts to rely on ‘capital flows’ that have ‘flowed’ into the deficit country is also misleading. That would mean viewing the loans taken out by French importers to buy German cars – because they had become cheaper due to German wage dumping – as the cause of the French losses. That is simply absurd.

What can be done about imbalances?

For many decades, it was undisputed that disadvantaged countries were naturally entitled to defend themselves against artificial and unjustified advantages and to protect their companies from the associated disadvantages. Consequently, in accordance with World Trade Organisation rules, one can introduce one’s own tariffs, devalue one’s own currency, or initiate anti-dumping proceedings against countries that support their domestic companies. Political pressure on one’s own wages to offset the foreign wage advantage in fixed exchange rate systems is also a possibility.

In the past, the simplest solution was usually to accept a devaluation of one’s own currency as soon as a balance of payments crisis arose. If a country found itself at risk of no longer being able to finance its own imports without incurring large interest rate premiums on the capital market, the solution was usually sought in a devaluation, whether under flexible or adjustable exchange rates (such as in the Bretton Woods system or the European Monetary System, EMS). This reduced imports, strengthened the country’s own exports and thereby reduced dependence on the capital market.

Flexible exchange rates were and are not a solution to imbalances, because currency speculation regularly produces distorted prices. Fixed exchange rates also have their pitfalls. Fixed exchange rates are, so to speak, a promise by trading partners not to undercut one another in any way, so that the option of changing the exchange rate would become necessary. The tighter the exchange rate peg, the firmer the trading partners’ promise not to undercut each other must naturally be, for the system to hold. Within the European Monetary Union, Germany has opted for the mercantilist form of undercutting, namely by tightening its own belt. This has broken the promise underlying the agreement to enter into a monetary union. Under sensibly drafted agreements, trading partners would therefore no longer be required to adhere to the principle of free trade; instead, they could impose import duties on Germany to offset German dumping.

The G7 paper draws the following conclusion:

“A current account deficit is not merely a trade imbalance – it reflects a gap between domestic savings and investment and is financed by net capital inflows, which over time accumulate to form the country’s net international investment position.”

My conclusion could not be more different:

A current account deficit is one indicator among many of the existence of an imbalance in international trade. An imbalance between saving and investment cannot be inferred from the existence of a current account balance. The fact that a deficit is financed by loans is a triviality. The loans that must be taken out by economic agents in the deficit country are referred to in balance of payments statistics as “net capital inflows”, but this is purely an accounting matter and has no economic significance. No capital flows from the surplus country to the deficit country.

The logical constraint

I must add one more thought, which many colleagues consider somewhat abstract, but which I find immensely important. There is a logically compelling reason why saving and investment can never explain current account balances. Let us imagine that all countries in the world had similar savings plans, for example, the desire to save more in order to provide for the future. Then there must necessarily be a mechanism that ensures these savings plans are brought into line with the logical necessity of creating an absolutely balanced current account for the world.

The race for current account surpluses is (unlike total trade) a zero-sum game for all countries in the world. Some countries must therefore necessarily abandon the idea of generating current account surpluses through increased saving. How does this happen? What mechanism exists to correct these inconsistent savings plans? Neoclassical economics has no answer to this whatsoever. It ignores this problem and is thus out of the running as a serious economic theory. But many Keynesians, too, have one large or several small gaps at this point instead of a logically compelling explanation.

The mechanism that brings the global current account balance to zero, despite otherwise planned savings targets, can—and this is logically compelling—only be a mechanism that itself has a zero-sum character, i.e. always takes from one what it gives to another. The two most important mechanisms of this kind are changes in the terms of trade – that is, changes in the ratio of import to export prices – and, closely related but not identical, changes in export prices (expressed in international currency) relative to one another, i.e. what is known as real exchange rate changes (i.e. changes in the competitiveness of countries).

This means that, in a rigorous analysis, only price ratios in the broadest sense can ever be responsible for current account balances