Eastern Europe has become the talk of the political town. While it was hoped in the West that the region would become a new power house in Europe after the Great Reunification in the early 1990s, from which the West would then also benefit, disappointment now prevails. The region is characterized by the emigration of many workers, the dominance of Western companies and enormous political instability, even the open turning away from Europe. What has happened?

In the West, people are content to express their displeasure at the insubordination of some governments, without even attempting to understand the results of the system change, which have obviously failed or at least fallen far short of expectations. This follows the tried and true motto: Those who are not happy and satisfied in the wonderful free-market system we have given them simply have only themselves to blame. From this point of view, political upheavals are the result of inadequate institutions and “corruption”. All economic failures in Eastern Europe, which Western European politicians and mainstream economists cannot or do not want to explain, are blamed on corruption, as they were in Southern Europe before, without any further search for the cause. Thus, a culprit has been found and there is no need to think further about one’s own mistakes.

Hungary was the first to show Western failure

Victor Orban was the first to draw Western ire because he did not see the rules of the Western system as having no alternative, but wanted to go his own way for his country in view of the power he had won in democratic elections. This is interpreted in the West as pure arbitrariness, because they never took note of how Orban came to power and what the West had to do with it. Victor Orban came to power again in 2010 (he had already been prime minister in a relatively inconspicuous manner at the turn of the century) because the mass of Hungarians had seen the ugly face of capitalism up close before and during the great global financial crisis of 2008/2009.

Across Eastern Europe, real estate loans in Swiss francs (or Japanese yen) had been granted by Western (mainly Austrian) banks in the name of free movement of capital. This was because interest rates in these currencies were extremely low compared to Eastern European interest rates. Thus, many Eastern Europeans borrowed in a currency other than the one in which they received their earned income. No one explained to them in advance what this meant, namely participation in speculative transactions on the foreign exchange market. The Western banks earned well from these credit transactions and had no interest in explaining to their new, inexperienced customers the risks of borrowing in foreign currency. After all, the sword of Damocles of exchange rate fluctuations permanently hovered over the interest rate differential between Eastern and Western Europe.

To make matters worse, the supposed hard currencies of the West were undervalued at the time of lending to Eastern Europeans, because speculation with Eastern European currencies had led to their completely unjustified revaluation. (This was associated with a noticeable loss of competitiveness of the Eastern European economies concerned). As a result, Eastern European borrowers had to borrow a relatively small amount in their own currency in order to be able to afford the loan in Swiss francs (or Japanese yen) – another strong incentive to borrow in these foreign currencies rather than in their own domestic currency.

Then, when the global financial crisis erupted in 2008, the currency relationships reversed. The Swiss franc and the Japanese yen appreciated sharply against Eastern European currencies, making mortgages more expensive in one fell swoop by orders of magnitude that were no longer sustainable for many homeowners. The situation was particularly bad in Hungary, where almost two-thirds of all households were affected.

This brought Victor Orban to power (with a two-thirds majority in parliament) because he promised to stand up for citizens at the expense of the banks. And indeed, in Hungary, by legal order, banks had to convert mortgage loans into forint loans at a reasonable exchange rate (rather than the market rate). In Poland, the intention was to leave the clarification of the ratios “to the market,” with the result that many affected persons filed lawsuits against their banks. As the Polish courts felt overwhelmed, they referred the case to the ECJ. The ECJ ruled in favor of the plaintiffs because they had been in a systematically inferior position in the negotiations with the banks.

The real exchange rate as a decisive indicator

In order to describe and analyze the undesirable developments in Eastern Europe that occurred before the financial crisis and are also building up again now, it is useful to look at the countries’ so-called real effective exchange rates. The real exchange rate indicates whether and by how much the competitiveness of an entire country is improving or deteriorating. It measures, for example, whether higher inflation in country A than in country B is offset by a nominal depreciation of country A’s currency against that of B. If this is not the case, or if it is not in the same range as country B’s, the real effective exchange rate is used. If this is not the case, or not to a sufficient extent, country A appreciates in real terms. This then means that all companies in the country lose competitiveness because they can only offer their products (at the same profit margins) at higher prices than their competitors abroad. Effective is the name given to the real exchange rate when it measures not only the value of one currency against a single other, but against a whole bundle of currencies, a so-called basket of currencies representing the currencies of the most important trading partners.

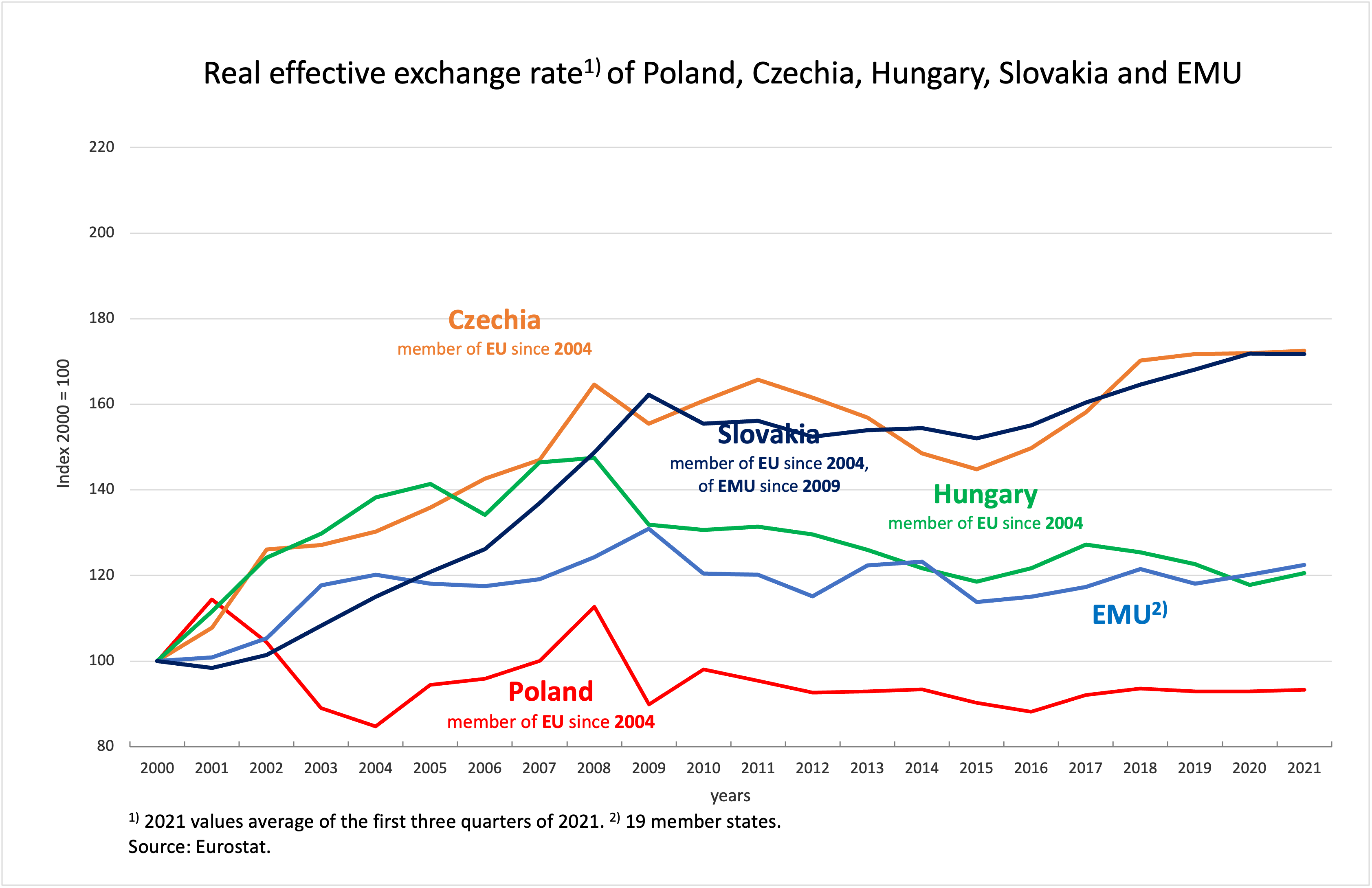

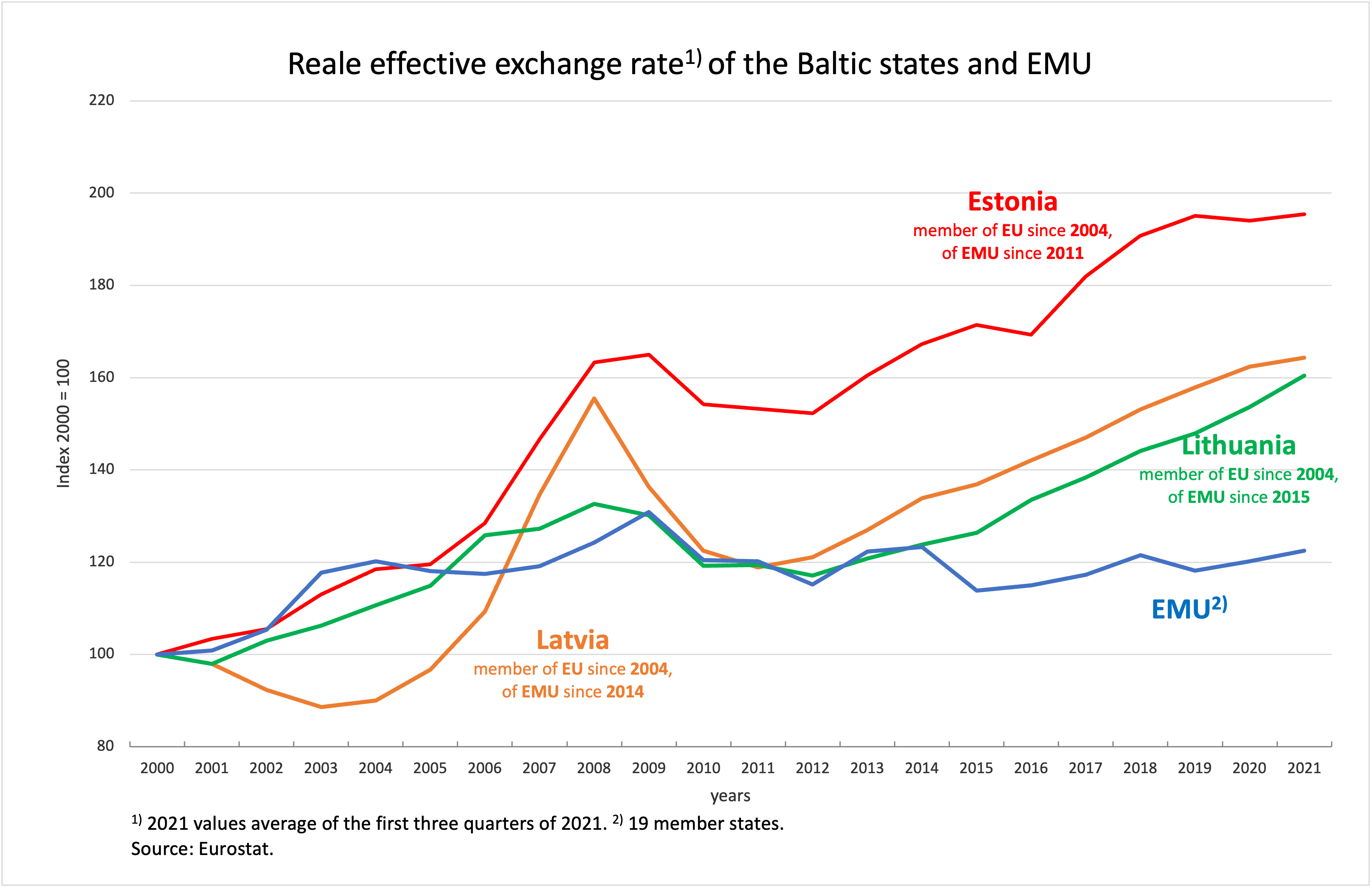

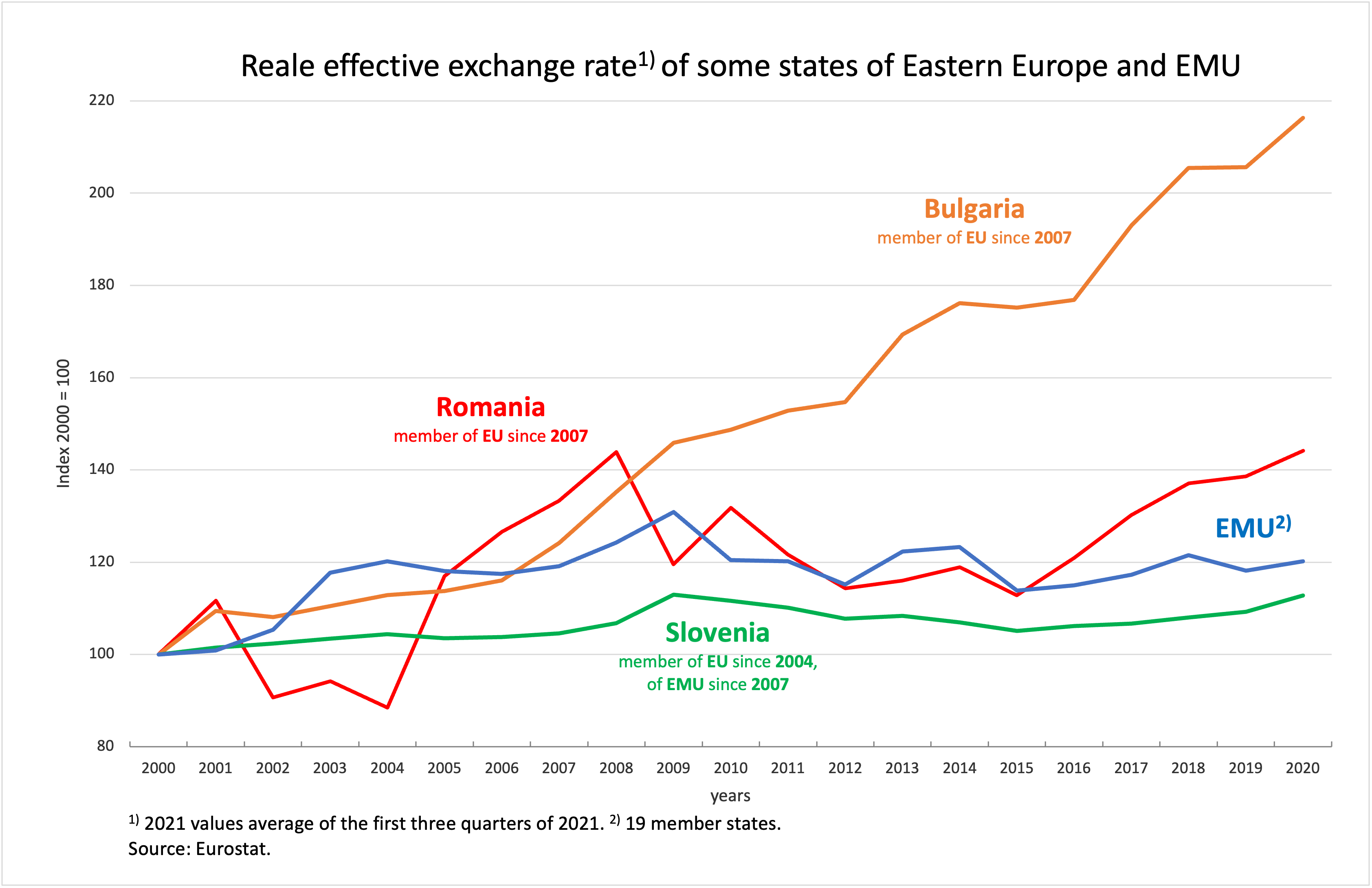

Figures 1 to 3 show the real effective exchange rate (REER) of various countries in Eastern Europe on a unit labor cost basis compared with the EMU.

On a unit labor cost basis means that unit labor cost developments have been used here to adjust the prices of nominal exchange rates. (The development of unit labor costs is understood as the difference between the respective national nominal wage change and the respective macroeconomic productivity progress). This type of price adjustment of exchange rates (instead of using inflation rates on a consumer price basis) is particularly suitable for assessing a country’s competitiveness from a business perspective because it directly reflects the cost situation of companies and thus the potential pressure on profit margins. This cannot be seen so well in price adjustments with consumer price indices, because it is not known whether companies are trying to maintain their competitiveness by making price concessions and are accepting a loss of profit in return.

Figure 1

Figure 2

Figure 3

In the Eastern European countries shown here, there is a fairly clear trend for real exchange rates: Over the past 20 years, they have appreciated against the EMU. The prominent exception is Poland, whose currency is now even slightly below its real value in 2000 and thus well below that of the euro area countries, which have appreciated in real terms overall. Similarly, Slovenia’s real exchange rate lags behind that of its EMU currency partners, but is somewhat higher than at the beginning of the century. Hungary’s currency has returned to the real exchange rate of the euro area after a long period of real appreciation until the financial crisis of 2008/2009. As far as the other countries are concerned, they lost competitiveness vis-à-vis the euro currency area during the period under review, and in some cases to a considerable extent.

Interestingly, this applies not only to EU countries such as Bulgaria or the Czech Republic, which have their own currencies, but also to EU countries that have joined the monetary union, such as Slovakia or the Baltic states. This is astonishing, since the applicant countries had hoped that this accession to a large monetary community would help them to escape the problems caused by “free” currency markets.

Even if one assumes that the respective real exchange rate (which is calculated only as an index to any base year) was balanced at the time of the respective country’s accession to EMU, i.e. identical to that of EMU, the current values of the real exchange rates of these countries mentioned are still significantly higher today than those of the entire monetary union.

And this is the problem of Eastern Europe: What should justify the fact that all companies in these economies are constantly facing declining competitiveness? Or to put it another way: How can it be that the development of the nominal exchange rates of the countries with independent currencies and the price levels of the countries that have introduced the euro has for years been such that, on average, their companies cannot keep up on the international markets?

At least in the case of the countries with independent currencies, this means that nominal exchange rates do not come close to doing what they should, namely reflecting the “fundamentals” of these countries to some extent correctly, at least in the medium term. In the “free” foreign exchange markets, this is precisely what does not automatically take place. On the contrary, in addition to the volume necessary for trade in goods, trade in the foreign currencies of these countries obviously leads a life of its own with considerable volume, which distorts exchange rates and at times pushes them in a direction that contradicts real economic realities.

And for those Eastern European countries that have abandoned their currency in favor of the euro or have pegged their own currency firmly to the euro, the visible and persistent loss of competitiveness means that monetary union is not working for them as hoped. (Incidentally, this is completely parallel to the difficulties experienced by southern European EMU members, suggesting that this is a fundamental design flaw in the monetary union). This is a bitter realization: neither the exchange rate results produced by “free” currency markets nor the abandonment of their own currencies solve the problem for the Eastern European countries of remaining competitive in the long run.

One would have to expect the currencies of countries with higher inflation rates to devalue again and again in order to close the price gap that has arisen at the expense of the country’s companies vis-à-vis more inflation-stable foreign countries. On the other hand, countries that have opted for a fixed exchange rate to the euro, such as Bulgaria, should be able to keep their unit labor cost and price increases within a range that does not systematically erode the economic base of the entire country. Neither, however, is the case in Eastern Europe, except in Poland and Slovenia and, after bitter lessons for some years, in Hungary.

The charts also show that the rising trend in real exchange rates associated with the global financial crisis of 2008/2009 was interrupted in some countries. The striking exception is Bulgaria. Obviously, there were shocks in the remaining countries that caused currencies to depreciate or abruptly interrupted wage growth. In Hungary, a huge exchange rate shock took place with a huge devaluation of the Hungarian forint against Western currencies. Hungary subsequently managed to prevent a resurgence of the previous trend of an inexorably rising real exchange rate. The exchange rate remained well below its previous maximum.

In the remaining countries, however, the real exchange rate has been heading upward again since 2015 at the latest, and thus into a region where the economy is bound to suffer major damage sooner or later. The developments in Estonia and Bulgaria are striking. Both countries have lost massive competitiveness since 2010; Bulgaria by 50 percent and Estonia by more than 25 percent. But by 2021, the Czech Republic and Romania are also already almost 20 and 28 percent higher, respectively, than the crisis-induced low levels of 2015.

What is happening in these countries?

The answer to this question is simple: wages are rising much faster than in the West. But they are also rising faster than the internal conditions in these countries, i.e., the national inflation rate and the national productivity trend combined.

Wages (compensation per hour worked) in Bulgaria, for example, have risen by an average of 7.7 percent per year over the past ten years, measured in euros. This is in stark contrast to the corresponding figure for Germany (+3 percent) and even more so for the EMU as a whole (+ 2.2 percent). The Baltic states are in a similar range to Bulgaria: in Estonia, the average growth rate over the past ten years was 6.9 percent, in Latvia 7.6 percent and in Lithuania 7.4 percent. Romania achieved an annual growth rate of 5.9 percent. The Czech Republic still manages 3.9 percent. Only Hungary and Croatia lag clearly behind their western competitors, with 1.7 and 1.0 percent respectively. Slovenia, at 3.1 percent, is roughly on a par with Germany, while Poland is slightly higher at 3.6 percent.

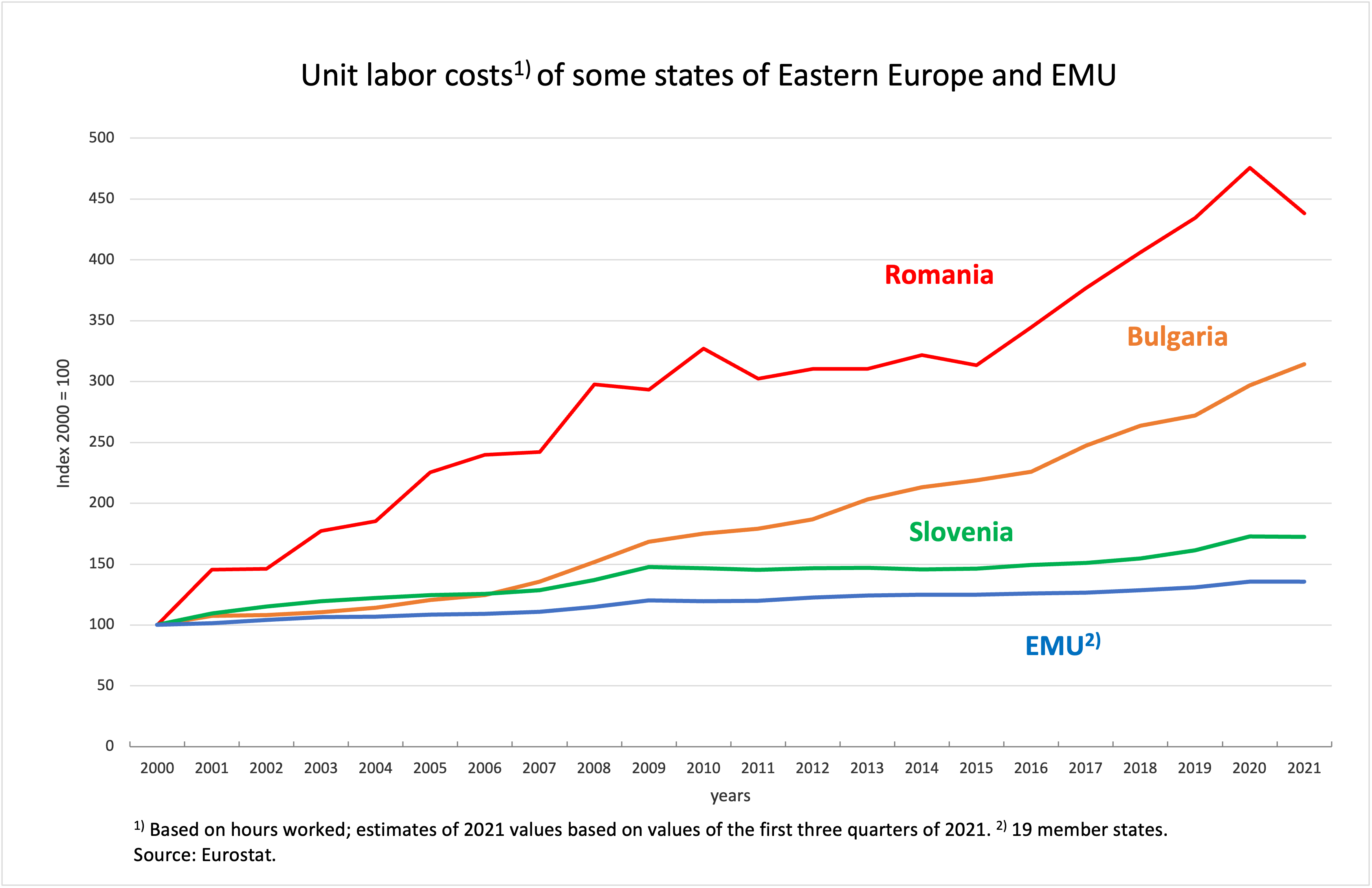

If the wage increases were underpinned by corresponding increases in labor productivity, the competitiveness of the companies in these countries would not be in danger. But this is not the case, as a glance at the development of unit labor costs in these countries shows.

Figure 4

Let’s start with the situation in Romania (see figure 4). There, unit labor costs have risen extremely – with fluctuations – for twenty years overall, more than quadrupling. In 2007, the country became a member of the EU. The increase in unit labor costs accumulated between 2007 and 2021 amounts to approximately 80 percent. If the country’s nominal exchange rate had not fallen by about a third over the same period, Romania’s international competitiveness would be even worse than it already is (see figure 3).

Bulgaria faces a tripling of its unit labor costs between 2000 and 2021. The increase since it joined the EU in 2007 is about 130 percent. This country also still has its own currency and could use the exchange rate valve to reduce the enormous loss of international competitiveness. However, it has chosen otherwise and has pegged its currency hard to the euro since 2007 with the result that the explosion in unit labor costs has largely passed through to the real effective exchange rate.

Slovenia, which joined EMU in 2007, thus completely abandoning the exchange rate valve, has been rather cautious about wage developments for years. The comparatively moderate increase in its aggregate unit labor costs fits exactly with the relatively favorable position of its real exchange rate.

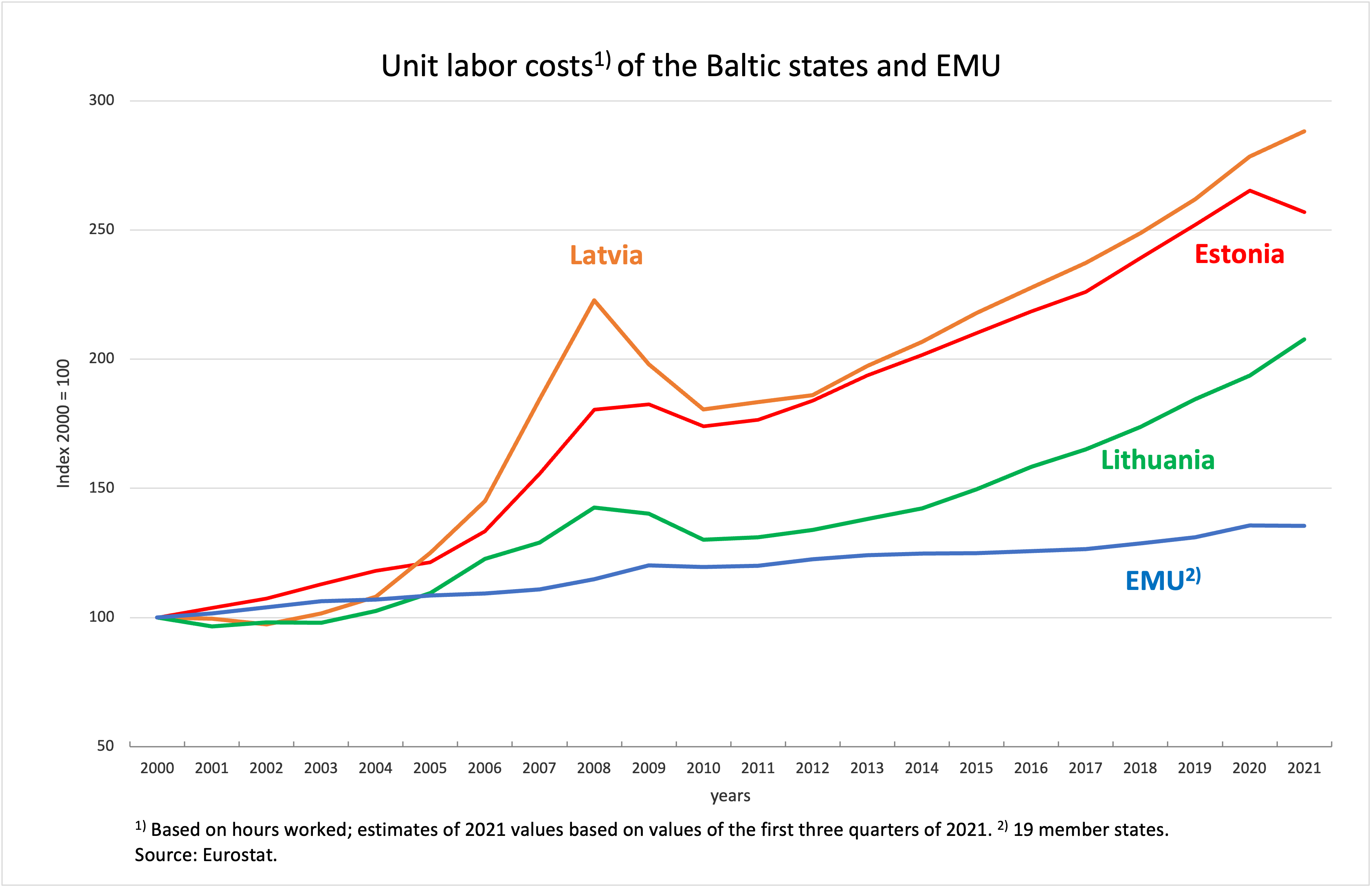

Figure 5

Figure 5 reproduces the data for the Baltic states, albeit with a different scale than in figure 4, so that the differences between the three countries can be better seen. Estonia and Latvia are hardly better off than Bulgaria, having gained more than 250 percent since 2000. Even after they joined EMU (in 2011 and 2014, respectively), their aggregate unit labor costs increased much more sharply than the Union average, by 45 and 39 percent, respectively (since 2011, it was 13 percent there, and just under 9 percent as of 2014). The same mistake was made by Lithuania, whose aggregate unit labor costs increased by 39 percent after it joined EMU in 2015, much more than the average for the currency partner countries (8 percent).

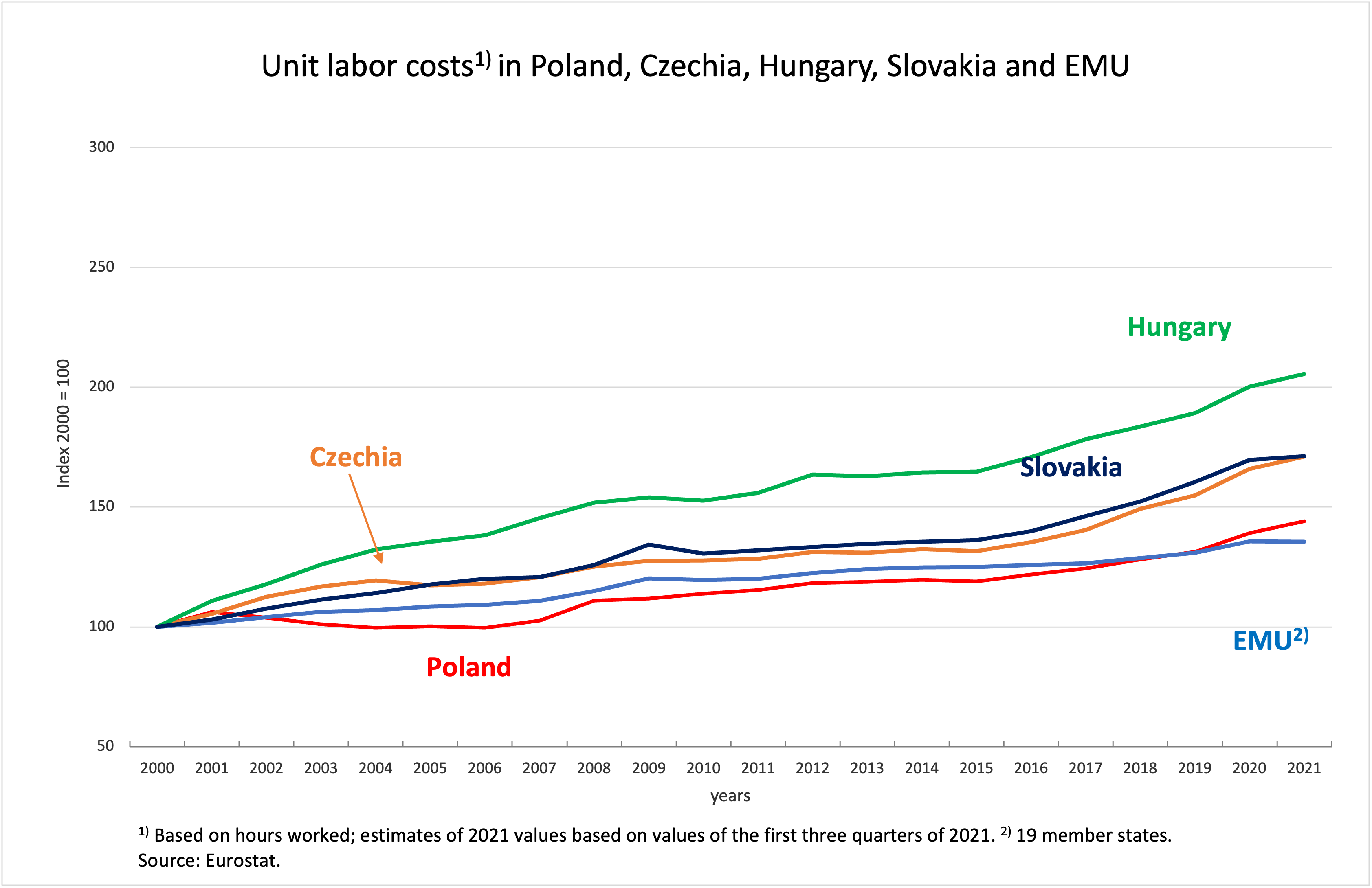

Figure 6 below shows unit labor costs for four other large Eastern European countries, only one of which, Slovakia, has adopted the euro, while the other three have independent currencies that they have not pegged to the euro. The scale in Figure 6 is the same as in 5 for the Baltic states. One can immediately see that only Hungary comes to a similar unit labor cost increase as the most cost “stable” Baltic country. And because it has allowed its currency to depreciate in nominal terms, it has now been able to converge with the international competitive position of the EMU states, as evidenced by its real effective exchange rate (see figure 1).

Figure 6

Poland has succeeded in strengthening its international competitiveness by keeping unit labor costs almost in line with the EMU and at times even lagging behind it. The Czech Republic and Slovakia, on the other hand, have experienced stronger cost development, which has caused both countries to lose international competitiveness: Slovakia because it no longer has an independent currency, and the Czech Republic because the Czech koruna has appreciated by a fifth in nominal terms against the euro since the country joined the EU in 2004, meaning that the foreign exchange market ignores the fundamentals of the real economy.

Special conditions in Eastern Europe

How can this be, one has to ask? Why is it that in most Eastern European countries the (traditionally weak) trade unions are able to achieve what their colleagues in the West simply cannot? The answer to this question is basically not difficult either, but the prevailing economic theory cannot provide it because it deals with equilibrium models and not with reality. If you look closely, however, you can see very clearly what is different in Eastern Europe than in the West: The economies in question are so closely linked to the West in two ways that they have very special production and wage conditions.

First, there are many Western manufacturing companies producing in these countries that have brought very high productivity to their production facilities and have them serviced by low-wage workers in Eastern Europe. As a result, these companies are making huge profits. The profit margins are many times higher than in the West – and higher than in domestic companies. These Western companies are also much less likely to resist high wage demands than their Western counterparts, because their profit margins allow them to cope with wage increases of ten percent for many years. Domestic companies are obviously hardly able to escape this wage pressure. They would probably lose their workforce if wages were significantly lower, because they would switch to better-paying companies with a Western background. So domestic companies are forced to go along with the wage settlements, which considerably reduces their profit margins.

Domestic service providers can presumably push through higher price increases because the services are not exposed to strong international competition. The state also goes along because the respective government has an interest in being able to show that domestic citizens are catching up with the West. Domestic companies, however, which compete with Western companies, especially on export markets, hardly stand a chance.

Second, those who cannot pay sharply rising wages must expect their workers to migrate abroad. In view of a huge absolute wage gap with the West, the inclination of young, well-educated people to seek their fortune in the West is high anyway. Bulgaria is the country with the fastest shrinking population in the world. If you don’t offer workers in Romania or Bulgaria prospects in the form of significantly rising wages, you hardly have a chance of finding well-trained employees. Again, the skilled trades and service industries will have to make ends meet with price increases, while the manufacturing sector will be lost.

The consequences of this development are dramatic, but they are by no means easy to see. Without the outflow, unemployment would be much higher, putting pressure on policy and wages. Without the exports of companies originating in the West, the respective trade balances would quickly be in deep red, and one would notice that something is fundamentally wrong. Even the growth rates do not look bad yet, because consumption is strong with the rising wages and the export surpluses of the Western companies also have a positive impact on the calculation of GDP.

Why are the politicians failing?

With the role of Western companies and the importance of outward migration, traditional indicators of a country’s success or failure are now of limited use. Eastern Europe’s national governments lack the experts to make international comparisons and draw conclusions. The EU Commission, which clearly has the task of advising and accompanying these countries, fails completely because, in its neoliberal credo, it refuses to acknowledge that the transition to a market economy was not a success story for Eastern Europe. If one reads the reports of the EU Commission on the economic situation in these countries (to be found here), the usual criteria are simply consulted, and consequently the countries are consistently attested a good economic performance.

What enormous and dangerous structural changes are taking place behind the façade of national accounts is not taken note of. One day, Western companies will leave because wage equalization is largely complete and they can produce more cheaply elsewhere, and these countries will be left completely bare and will depopulate even more.

However, unlike the European statisticians and analysts, the population has a very good sense that something is wrong. You can see the extensive dependence on foreign companies, you can feel the gaps in the population torn by emigration, you can feel the impotence of the increasingly fragile democratic institutions and the inability of their own government to bring about fundamental change. The result is general frustration, a turn toward nationalism and increasing questioning of democracy.