Cross-posted from Brussels Morning (https://brusselsmorning.com)

You could have guessed it: As soon as the end of the Corona crisis is in sight, the inflation alarmists of all countries come out of their holes painting horror scenarios of hyperinflation.

In the US, former Treasury secretary Laurence Summers has been particularly prominent, warning that the stimulus programme planned by the new Biden administration is too big and could consequently have undesirable inflationary side effects. For the US, where there is traditionally little fear of inflation, this is quite remarkable.

For Germany, where people have been systematically inculcated with fear of inflation for many decades, this is already the norm. There is not a month in which a charlatan who lets himself be called a ‘star economist’ or ‘top economist’ by ‘business journals’ does not come up with inflationary horror scenarios that are only intended to drive investors into gold, stocks or Bitcoin because the ‘top economist’ presumably earns good money from them.

Mainstream economic thinking

But even economists, who we trust to have good judgment, are regularly fundamentally wrong. They warn that high rates of money supply growth will inevitably lead to inflation if growth is weak.

That expectation is false, however, because the supply of money does not determine how it is spent in the economy. In sum, supply does not guarantee circulation when there is zero growth.

Even more problematic is the argument, heard repeatedly, that there has never been inflation without expansive monetary policy. The assumption is that long-term expansionary monetary policy can only end in inflation.

But this is a serious logical error.

Without fail, printing money is a necessary condition for inflation. But more money is not a sufficient condition for surging prices. That is like someone claiming that the cause of speeding and ensuing traffic accidents can be blamed on the fact that drivers have a car.

What gets lost in most discussions of impending inflation is the central question of whether or not event timing allows the central bank or the government to respond in a timely manner to any threat of inflation. Economists are generally not very good at answering such a question because they are used to giving impulse-response answers rather than thinking about trajectories in real time. They do comparative statics: they compare the state of an economy (or model of an economy) before and after an inflationary impulse.

What we know precisely is the long-run cause of inflation, which is wage growth.

The relationship between inflation and unit labour costs is incontrovertible. If nominal wage costs rise more than labour productivity over 10 or 20 years, this is largely reflected in the inflation rate of the country concerned.

However, the mainstream economist is not ‘allowed’ to use this relevant and empirically documented and verified inflation theory, which would make a huge contribution to enlightenment, because it would challenge a central myth, namely the flexible and self-regulating labour market.

A sensible scenario

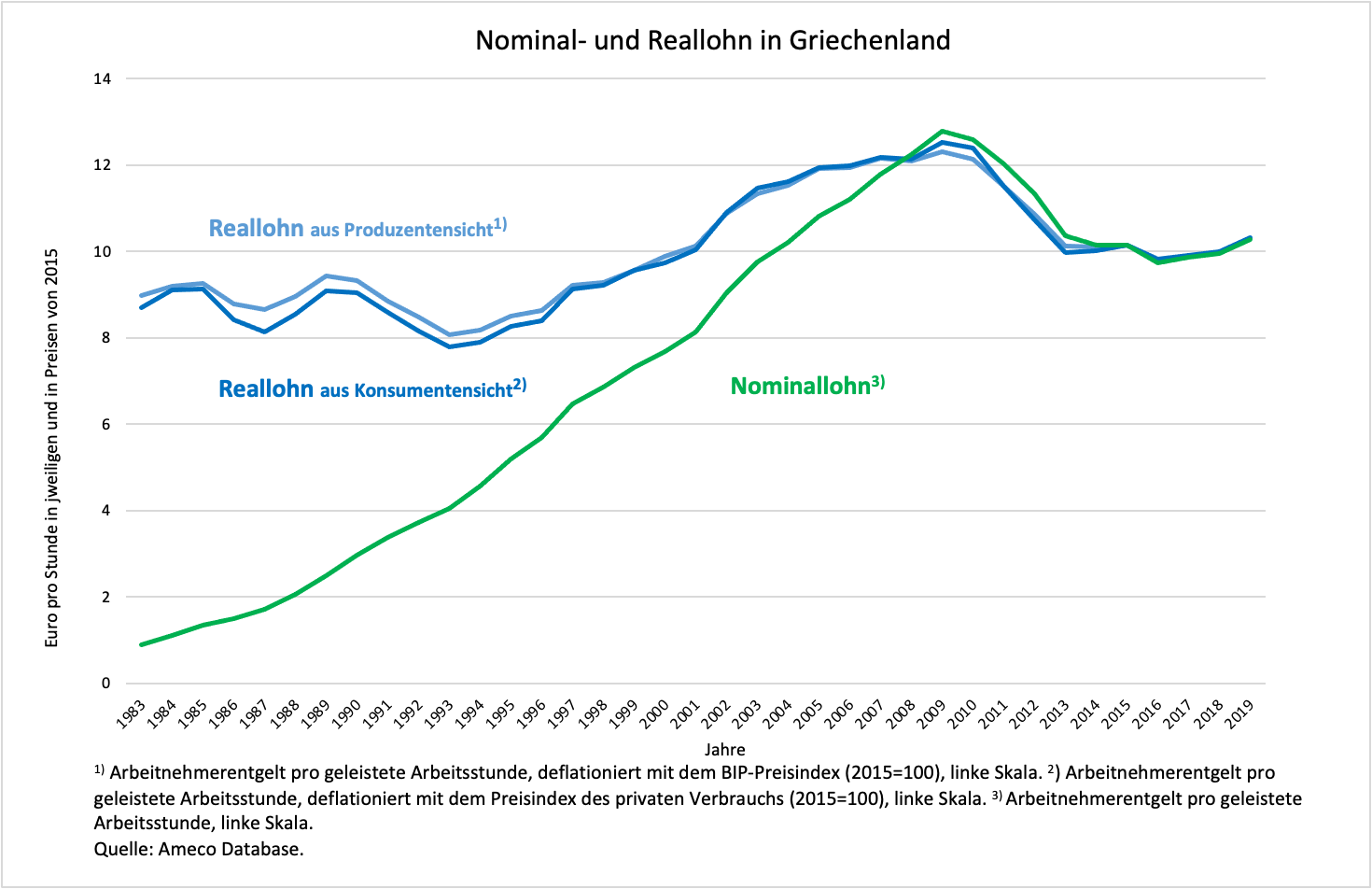

The stable long-term relationship between income and inflation does not correlate perfectly in a specific time frame. A classic counterexample is Greece where, after 2010, where there was a massive nominal wage cut – demanded and enforced by creditors – that did not yield a proportionate drop in inflation (Figure 1). Normally, if inflation fell along with incomes, “real wages” would have remained stable. That did not happen.

Figure 1

Now, the relationship between employment and prices may work in the sense of “price flexibility”. In sum, companies may be able to exploit their strong position to quickly adjust prices to rising wage costs. But high wage increases are simply not to be expected when the economy booms. Globally, there has been a massive increase in unemployment during the pandemic, weakened workers’ and unions’ bargaining position, where they retain any bargaining power at all.

The eruption of the Coronavirus pandemic found the US with historically high levels of employment, in an economy where observers noted that near-full employment did not translate into wage increases. Why should it be easier to push through wage increases now, after a significant increase in unemployment?

Don’t expect inflation when wages are low

All inflation processes take the route of higher wages.

There is no inflation that suddenly and unpredictably falls from the sky because the money supply has increased or the state spent more money than usual. That is why the time aspect is absolutely crucial in assessing the risk of inflation.

Let’s assume that there would be a strong upswing throughout the world starting in 2022. As a result, employment figures rise and unemployment starts to fall. Annual growth rate of 3% in industrialised countries, experience tells us, yields an uptick in employment of 1%. Currently unemployment in the eurozone affects 14 million people, close to 8.5% in a labour force of about 160 million. To subdue unemployment to a level in which workers have a better bargaining position, the unemployment rate would certainly have to fall to well below 5%. One should recall that even in Germany wage growth has remained weak despite better employment figures than in the rest of Europe.

To achieve this, the number of people in employment would have to increase by a total of six million. That is without event taking into account “hidden” worker reserves, i.e., more people willing to work when employment conditions improve. Even in the rosiest of scenarios with 3% growth we would create 1.6 million employment positions each year, which means there will be four years before needing to worry about workers’ bargaining position and inflation. If workers did improve their bargaining power in a Europe in full employment, unlike the US, it would take another few years to drive wages up to a point of concern.

Let’s not solve problems we don’t have

Who could and would prevent the European Central Bank (ECB) from raising interest rates at that point? After almost 10 years of upswing and the return to full employment, who would stand in the way of the ECB ensuring that wage policy does not overreach by hiking interest rates? The ECB has all the time in the world to prepare for this eventuality and prepare in small steps so as to avoid collateral damage. One of the options at that point would be to raise the yield it charges for the stock of government securities it currently holds.

However, such a sensible development is not likely. There is little to suggest that Europe could succeed where it has repeatedly failed this century, namely, to overcome its neoliberal mental block, driven primarily by Germany. After all, one would have to overcome the debt phobia in Berlin and recognise that in a world with companies that are net savers, even in a zero-interest environment, the Maastricht Treaty debt rules are both obsolete and dangerous. And all European countries would have to be given the flexibility to run public debt commensurate with their own macroeconomic circumstances and not with arbitrary criteria written into a treaty. That would be a miracle.

Anyone who does not believe in miracles must believe that interest rates will remain at zero for the next 10 years and that the inflation rate will remain close to deflationary levels and well below 2%, apart from small and short-term fluctuations, of course.