Cross-posted from Brussels Morning

Many German economists still blame the European Central Bank (ECB) for doing what central banks normally do, namely providing monetary conditions that are conducive to growth and development.

Particularly damaging for the public debate on how to exit the corona recession are the constant warnings by many economists and some doomsday prophets that the aggressive monetary policy within the monetary union risks triggering imminent and dramatic inflation throughout Europe.

Because criticism of the ECB is part of the etiquette, even in leftist circles, the field is wide open for those hyperventilating about the spectre of hyperinflation with arguments based on long-disproved monetarist theses.

Managing Debt

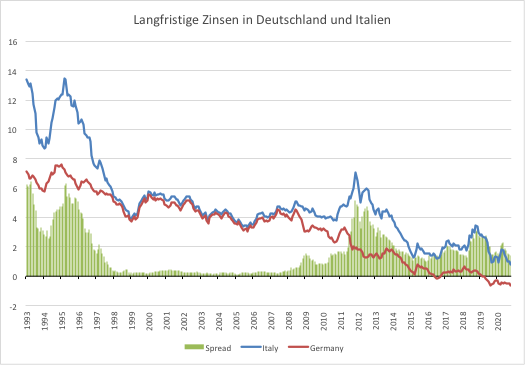

The quiet manner in which the ECB has managed to keep spreads (the interest rate differentials between countries on government bonds) low (Figure 1), enabling all member states to finance their new debt smoothly in spite of the difficult legal and political conditions thrown up by this crisis, has hardly been noticed, much less credited.

Figure 1

Italy may have to pay more than Germany, but the gap is small and at around 1%, Italian interest rates are also low in absolute terms. Under these circumstances and with a reasonable European debt rule for the future, Italy would not need the European bailout plan devised this summer.

However, individual Member State national budgets are of limited significance if it is not capital markets but the ECB that determines the terms of refinancing. This is exactly what the ECB does. The principle that the ECB must not finance government debt that was enshrined in the Maastricht Treaty – and still vehemently defended by Germany – is now little more than a fiction.

Harder ‘’to short’’ EMU member-states

We have reaped the full benefits of the European Monetary Union (EMU) because of the ECB’s pragmatic policy approach following the shock of the coronavirus pandemic. Had each individual country been forced to try to finance itself in capital markets, they would be easy picking for market speculators.

Speculators would have mercilessly targeted the national currencies of the countries, which, for whatever reason, would have been identified as candidates for devaluation. Such currencies would have been sold (“shorted”, in the parlance of the financial markets) and thus put under pressure to devalue.

Such a purely speculative and unjustified devaluation can easily get out of hand to a point where the mass of citizens lose confidence in their own currency and flee to other currencies.

People then pay their taxes in their own currency and use it for daily shopping, but they no longer trust it for longer-term transactions. No government or central bank can want that. However, they cannot prevent it as easily as the ECB can prevent a rise in long-term interest rates.

Foreign exchange reserves are always limited. Without them, states cannot intervene to buy their own currency to support its value, a fact that speculators are aware of and alert to. Look at the current dilemma in Turkey where, in the middle of a severe recession, the central bank has raised interest rates significantly to protect its own currency from another drop against the euro and the dollar. In doing so, it is accepting the fact that the interest rate hike will cause serious damage to the Turkish economy.

This proves the advantage of a large currency union. Nobody speculates against the euro or the dollar on a large scale, because every insider knows that the two most powerful central banks in the world can inflict huge losses on speculators in a concerted action within minutes.

In addition, speculation in foreign exchange always requires at least two currencies: a relatively stable one, in which one is in debt or has assets, and a less stable one, which one enters in order to collect high nominal interest rates and possibly exchange rate gains.

If a large country like the United States or a large block of countries like the EMU with a single currency has a lower inflation rate and – relatively speaking – greater economic stability than most of the rest of the world, why would anyone want to speculate against their currency? For one thing, “devaluation” would require a more stable currency.

At the moment, the only candidate would be the Swiss Franc, which is precisely why the Swiss central bank systematically intervenes to weaken its own currency. The logic is the same as with competitiveness: without a reference currency that is seen as overvalued (not-competitive), there is nothing to exploit and therefore nothing to earn without actually making a productive investment in the real economy.

In view of the enormous advantages that a large and stable monetary union offers in such a crisis, it is all the more regrettable that Germany, with its nonsensical policy of persistent current account surpluses and its outdated economic policy doctrine is preventing the EMU from becoming a success story not just as a currency but also as an engine for European domestic development.