This week will probably prove it once and for all: the Europeans are mad. The Americans, on the other hand, although generally considered mad, are finally leaving the Europeans far behind when it comes to economic sense. On Thursday, the ECB Governing Council will meet and, unless all the forecasters are wrong, will raise interest rates, even though the European economy is in the doldrums. In the US, which is still enjoying strong growth, full employment and rising labour force participation, the President is, by contrast, pressing the Federal Reserve to cut interest rates.

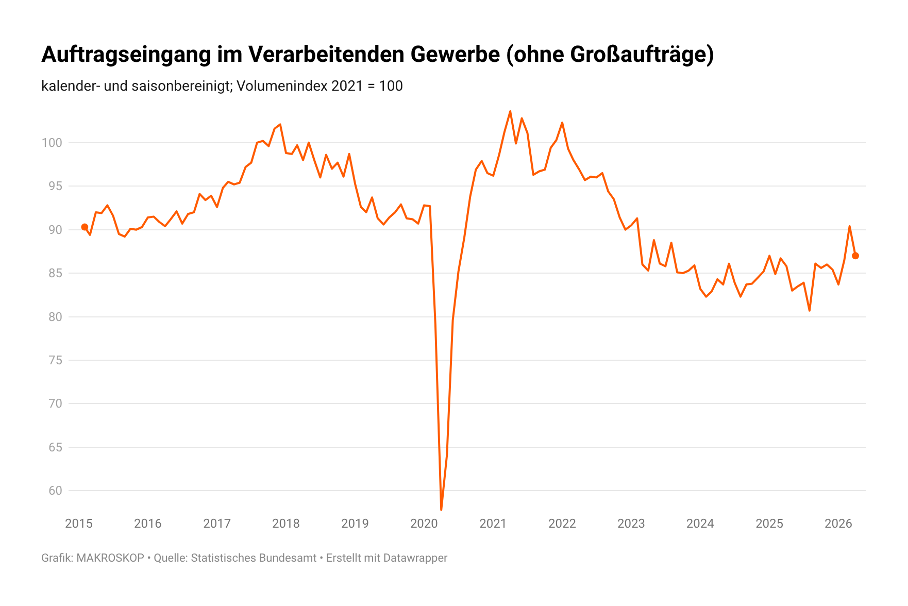

For the German economy, after all the largest in Europe, there have once again been extremely sobering figures this week. Industrial order intake remains at recessionary levels. Figure 1 shows that incoming orders, excluding bulk orders, fell again in April, after things had looked slightly better for two months. This figure also shows what the German economy has consistently been lacking since 2017: Demand!

German recession since 2017

If one draws a line through the Covid period, cutting off the two peaks at the top and bottom, it is impossible to overlook the fact that the downward trend, which began as early as 2017, has now become trapped at a low point that is almost 15 per cent below the 2017 level. This is a glaring and persistent lack of demand, which the universally sought-after ‘reforms’ can only exacerbate, but never resolve.

Figure 1

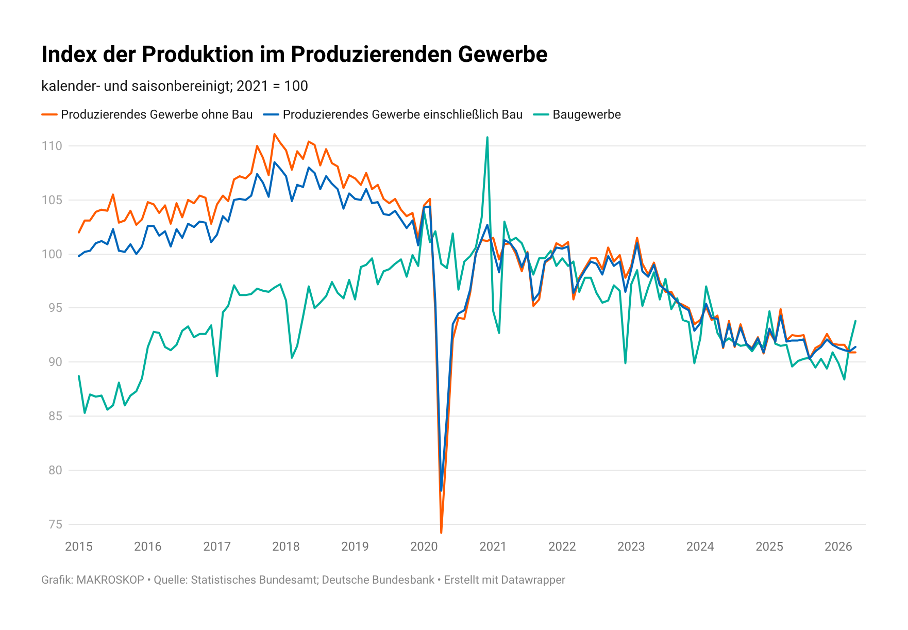

Even more clearly evident is the seemingly unstoppable decline in manufacturing output in Germany. Since 2023, production in this sector – which is crucial to the economy as a whole – has fallen almost steadily and continuously, having previously stagnated for several years. I have already pointed out elsewhere that, in view of this development, the Federal Statistical Office’s GDP estimate for the first quarter of this year – at plus 0.3 per cent – is a pipe dream that, once again, bears no relation to reality.

Figure 2

Anyone who expects an economy in this state to withstand an interest rate hike cannot, I must put it this bluntly, be in their right mind. Yet, unfortunately, this is precisely what must be said of a large number of members of the ECB Governing Council. They have become entrenched in an analysis that has nothing to do with reality. Some Governing Council members – and, regrettably, the two Germans, Nagel and Schnabel, are right at the forefront of this – are downright obsessed with the idea that the ECB might once again miss the ‘inflation’ target. Yet this is even more far-fetched this time than it was in 2022 and 2023, when there were also external shocks for which no one in Europe was to blame. Consequently, a tightening by the ECB can only do harm, without being able to change anything about the external shocks.

Let us assume for a moment that the current rise in fossil fuel prices would lead to consumer prices in Europe rising by three per cent at the end of the year, rather than the two per cent targeted by the ECB. For consumers, this means a one-off loss of real income, because oil and gas producers will record a corresponding profit. If there is no new external shock, the inflation rate will settle back at two per cent after a year – without any further intervention from any quarter.

If the central bank raises interest rates before the end of the year, the already extremely weak economy will be further damaged, without this altering the fact that the price effect will eventually fade. Consequently, the negative interest rate effect increases the likelihood that the real incomes of the majority of consumers will fall even further and that unemployment will rise more sharply than it would otherwise.

Second-round effects?

The central bank’s intervention is regularly justified by the risk of so-called second-round effects. It is claimed that even in the case of a brief shock, inflation could rise more sharply than expected because businesses and employees behave irrationally. They want to avoid losses in purchasing power and therefore demand higher prices or higher wages. This could lead to inflation remaining permanently above the target level, even if the original energy shock has already subsided. To prevent this, according to a conclusion by the Central Bank Council, the central bank must intervene early and vigorously.

This argument, repeatedly put forward by central bankers, holds no water whatsoever. In a democratic society where there is open communication, even the technocrats at the central bank cannot simply sidestep a strategy that is capable of achieving the same result at a significantly lower social cost.

Temporary, externally induced shocks that reduce purchasing power cannot, it seems, be prevented by any available economic policy means. The state can, admittedly, absorb the costs in the short term by taking on additional debt, but even then these costs must be borne by society. If, however, the state allows market prices to take their course, domestic distributional conflicts cannot be ruled out. Yet it would be foolish to shift the burden from one group to another – that is, from the trade unions to businesses, and from businesses back onto workers via price increases.

If policymakers recognise this scenario, in which everyone ultimately loses out, they should intervene and discuss with all stakeholders (including the central bank) just how dangerous domestic distribution conflicts are, particularly given that central banks could use them as a pretext for raising interest rates. But politicians must also make it clear to central bankers that, despite their independence, they do not come from another planet and must not accept social costs that could be avoided if all parties involved behaved sensibly.

As early as 2022, the ECB overreacted to a temporary surge in prices. The central bank acts as if from another planet and clearly ignores the macroeconomic dialogue envisaged within the EMU (in 2025, for example, there was no statement from the ECB, as can be read here). Will the ECB – due to an inability to communicate with one another – repeat the same mistake as in 2022/2023, and will the European economy be set back by years once again because a technocratic organisation refuses to understand its social responsibility and the relevant economics?

What politicians must do

Should the ECB refuse to enter into talks, European policymakers should make it clear to the monetary policymakers that they will not allow the recession to worsen. An intellectually sovereign state can – as the US is currently demonstrating – offset an interest rate hike through its own stimulus measures.

Politicians would have to make it clear to central bank officials that they will not go along with the central bank’s recessionary logic from the outset.

The state must keep an eye on the functioning of the entire system. This goes far beyond a one-sided and narrow-minded stability policy. Europe as a whole is at risk if it does not succeed in steering economic development towards expansion in the foreseeable future. The ECB, too, is politically finished if there is no longer any acceptance of European integration and European responsibility in an increasing number of European countries.

However, politicians – including via the ECB – are being threatened by the markets. The markets could boycott the government bond market and drive up interest rates. After all, long-term interest rates have already risen in recent weeks. Yes, interest rates have risen because, due to irresponsible comments by central bankers, the markets have become increasingly convinced that the ECB will raise interest rates. This only proves that the ECB is capable of doing the wrong thing even before an official decision is made, through nonsensical statements.

For the markets in Western industrialised nations, there is no alternative to government bonds. If you do not want to lend money to the state, you can hide your money under the mattress; there is no third option. Given the situation I have described hundreds of times – that private companies in all Western countries have been saving on balance for over 20 years – the state is the only player capable of providing a return on the hundreds of billions in savings that enter the market anew each year. Consequently, it is merely ridiculous speculation, triggered by the central bank itself, that is intended to frighten governments. Anyone who allows themselves to be frightened by this simply does not understand what is at stake.