No sooner had Javier Milei won the congressional elections with the help of unprecedented American interference in the election campaign than the libertarians regained the upper hand and once again celebrated the Argentine president’s economic successes, which do not even exist. Although the inflation rate is significantly lower than last year, it remains at a very high level of over 30 per cent. Economic development is disappointing. There are no signs of an upturn. Underemployment is severe and production figures show no signs of economic momentum. In July of this year, we presented the facts in a discussion of a scandalous OECD report, and the trend identified in that analysis still holds true today.

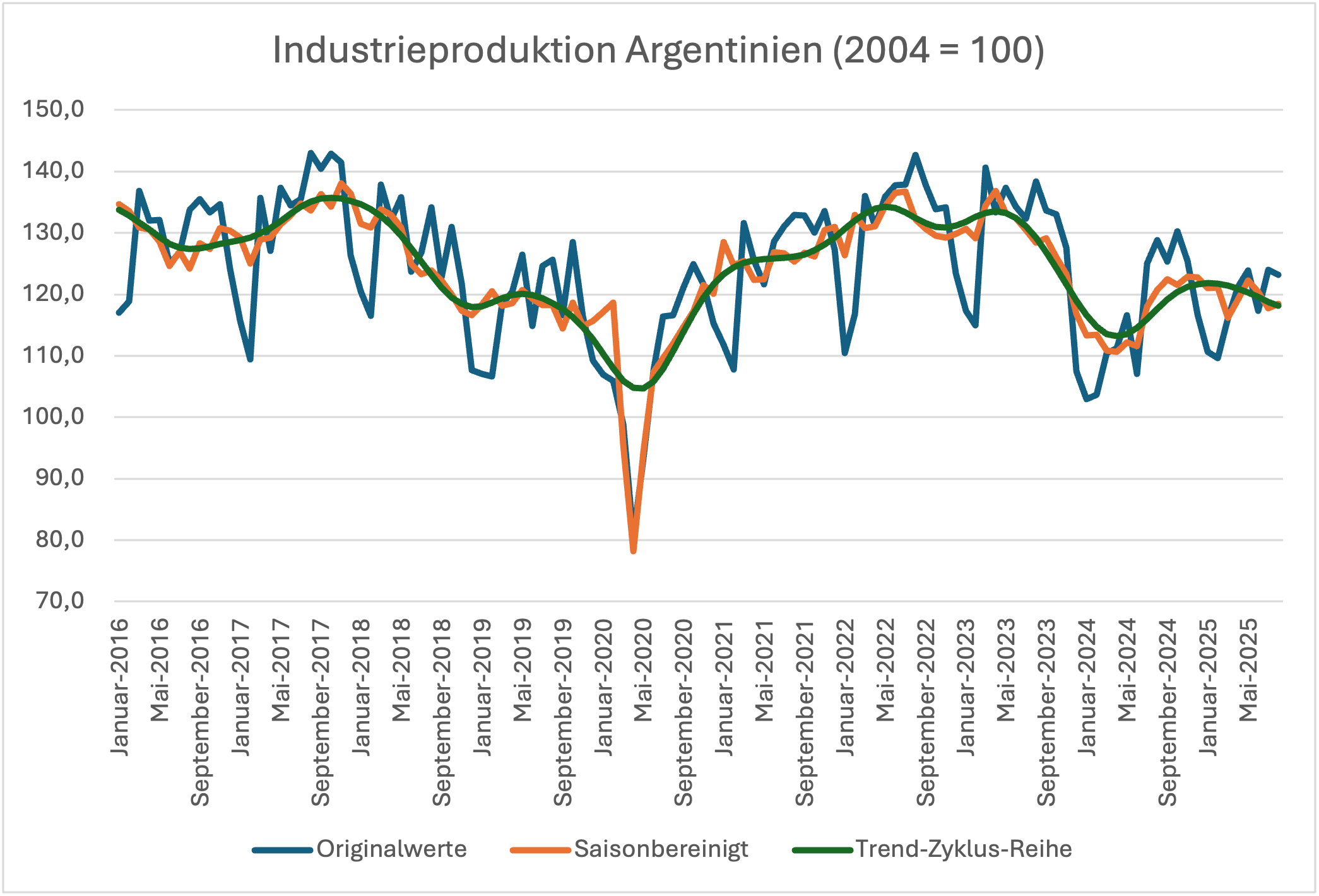

Figure 1 shows the development of industrial production up to August of this year. Shortly before Milei became president in December 2023, the index of (seasonally adjusted) industrial products was still slightly above 120; in August of this year, it stood at 118. In between, it fell significantly (by more than ten per cent) and then rose slightly again. Since the beginning of this year, it has fluctuated around the 120 mark, but has recently fallen below it again. Whatever else may be claimed, an economy with such a trend in industrial production is not in an upswing, but is struggling not to fall back into a deep recession.

Figure 1

Source: INDEC

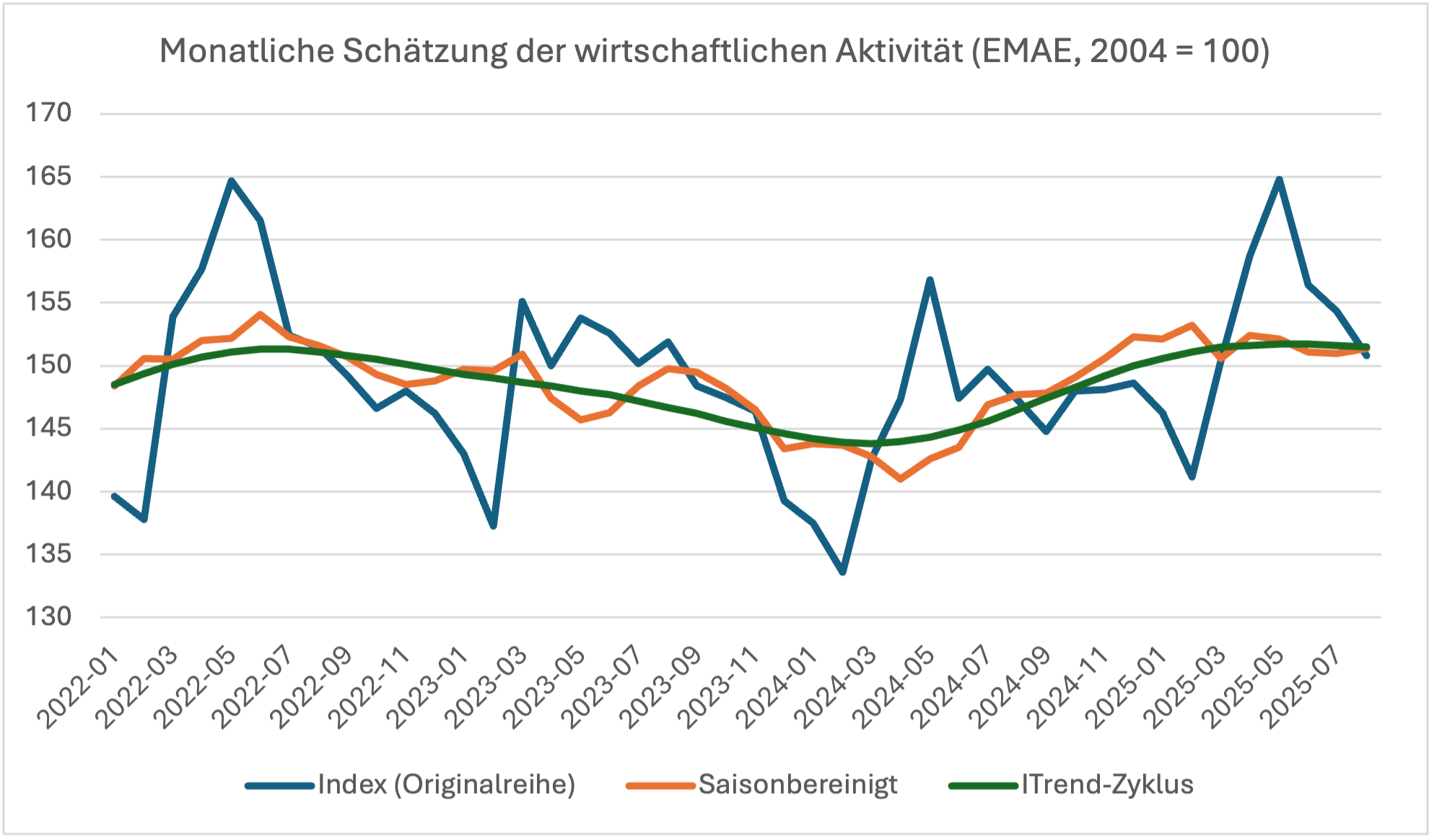

A similar and corresponding picture emerges when looking at the monthly estimates of economic activity (Estimador mensual de actividad económica (EMAE), Figure 2). This indicator, published by the Argentine statistics office INDEC, measures monthly changes in overall economic activity and thus serves as a leading indicator for GDP development. According to the latest data, the seasonally adjusted index value in August 2025 (2004 = 100) stood at 151.4 points, 0.3 per cent higher than in July, but only 2.4 per cent above the level of the same month last year. The trend cycle value (-0.1 per cent compared to the previous month) remained virtually unchanged, which means that, despite the sharp slump in 2024, the country has been in a state of stagnation since spring 2025. There is no sign of an upturn.

Figure 2

Source: INDEC

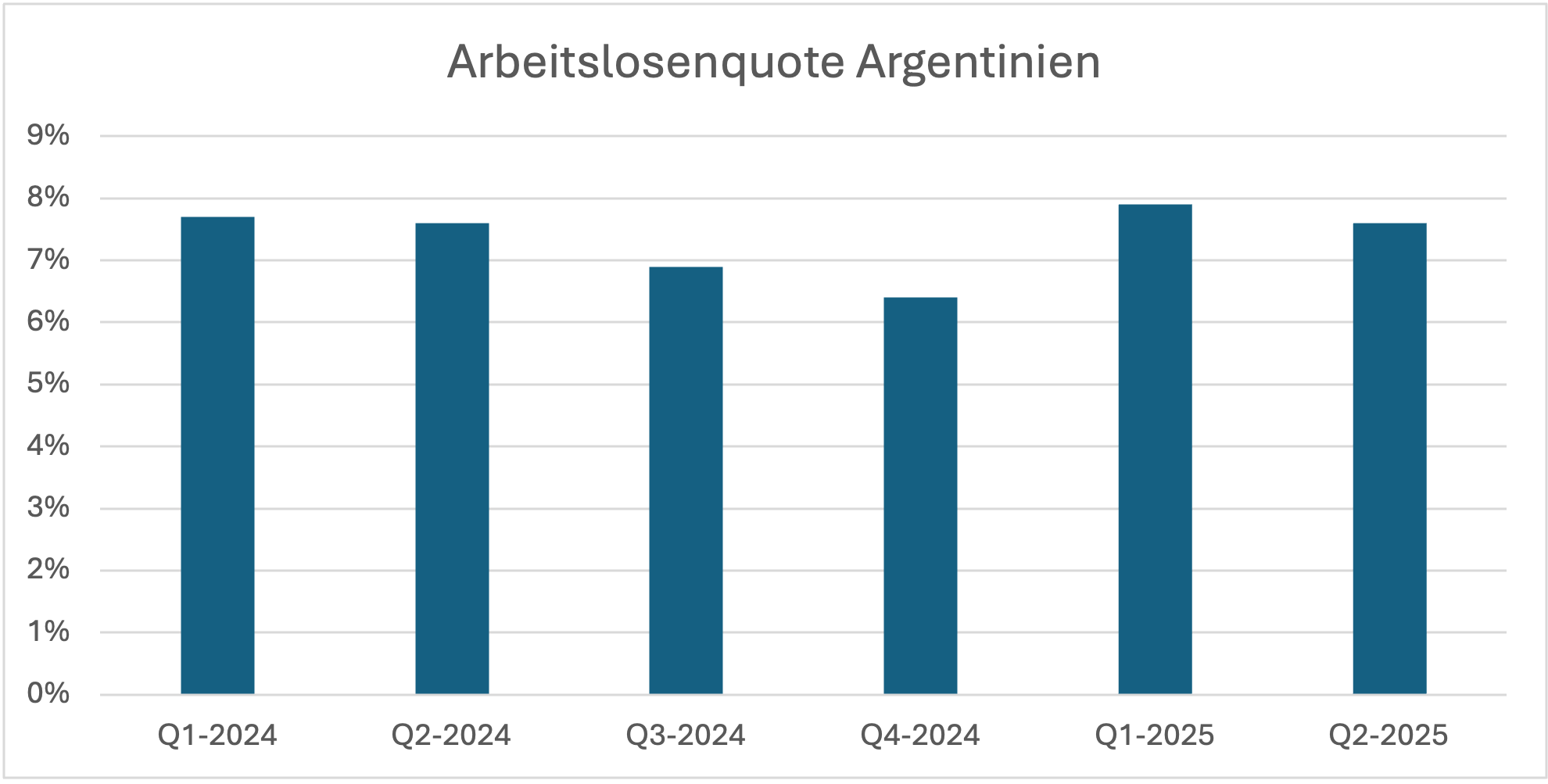

Unemployment (Figure 3) also points to weak development. The unemployment rate, which rose significantly in the first quarter on a seasonally adjusted basis, fell only slightly in the second quarter. According to INDEC, the underemployment rate, defined as the proportion of employed persons who involuntarily work less than 35 hours per week and would be willing to work more hours, was over ten per cent.

Figure 3

Source: INDEC

There is clearly no upward trend in the Argentine economy this year. The Financial Times wrote a few days ago: “Analysts say the government’s focus on lowering inflation began to weigh the economy down this year. Below-inflation wage increases negotiated with Argentina’s powerful unions in early 2025 reduced consumers’ purchasing power, while local industries shed jobs as the stronger peso and lower tariffs favoured imports.”

This is an accurate description. In our July report, we made it clear that the reduction in inflation is mainly due to wage moderation. It is almost inevitable that this will lead to a temporary decline in real wages, which in turn will have a negative impact on demand and the economy. The negative effects of currency overvaluation, which Milei has long relied on, were also to be expected.

Economic policy options reduced once again

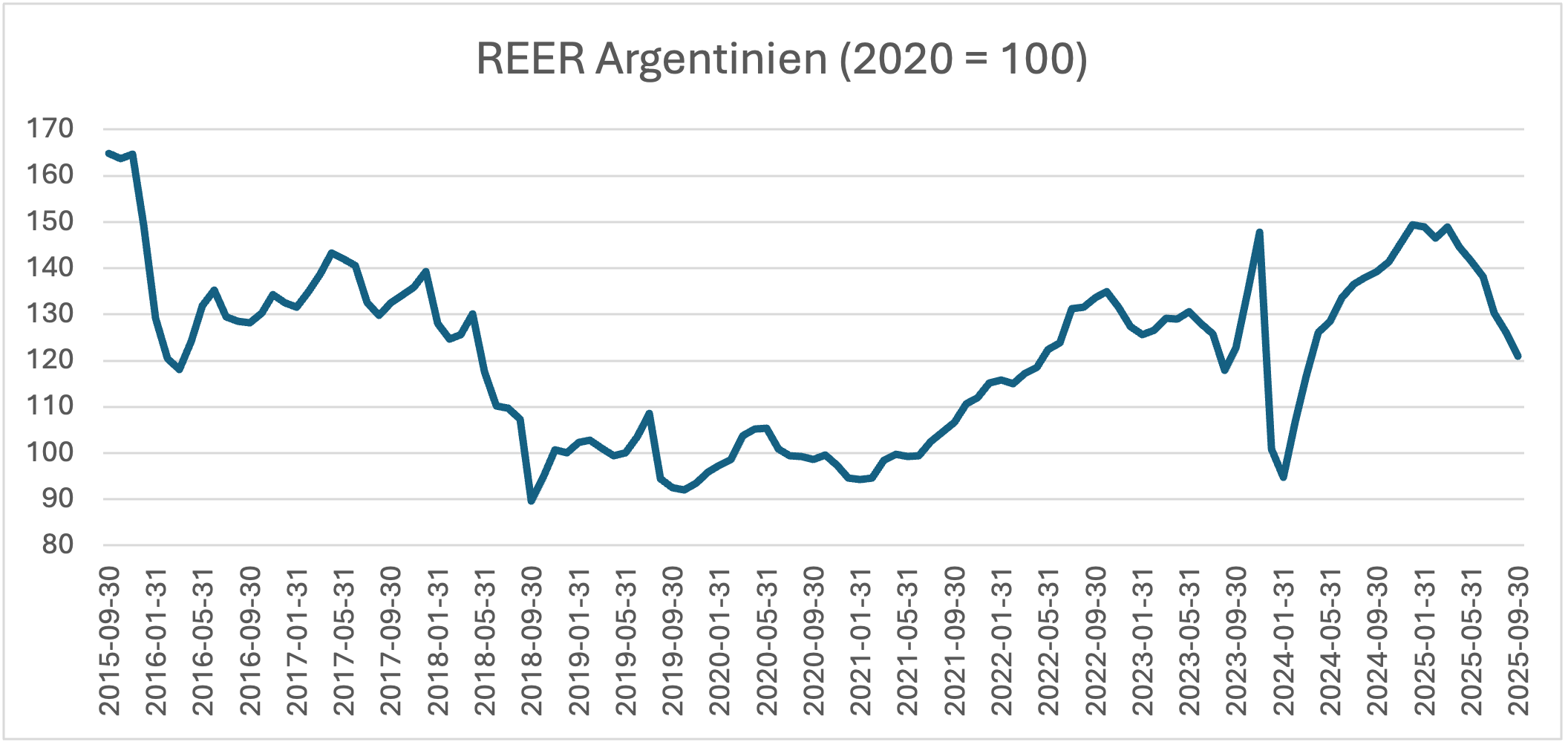

For this reason, and due to an acute shortage of foreign currency in the summer of this year, Milei abandoned his attempt to further support the Argentine peso. As a result, the peso plummeted, putting an end to the government’s attempt to reduce inflation by fixing an unrealistic exchange rate. Even the real exchange rate in Figure 4 has fallen by more than 20 per cent. But even this offers only short-term relief, especially since the real exchange rate is still well above the level of December 2023 and also shows a significant overvaluation compared to countries such as Brazil or Turkey.

With an inflation rate of over 30 per cent, Milei needs a nominal devaluation of this magnitude every year. However, this devaluation can never be achieved under orderly conditions by the markets that Milei so deeply admires. Speculation on interest rates and currency relations systematically prevents this (as shown here). That is why any advice that amounts to simply floating the currency, i.e. leaving it to the markets, is more than dangerous.

Figure 4

Source: BIS

Milei now needed international help because, naturally, he wants to prevent a massive and self-reinforcing collapse of the peso. He needs a devaluation, but one that remains quantitatively in line with the inflation differential between Argentina and its main trading partners. This is not possible without intervention, and intervention is not possible without foreign exchange. However, the country no longer has any foreign currency, which is why help from the US (or the IMF) is inevitable. Contrary to its usual practice, the US has promised him this help because he is ideologically on the same wavelength as the Trump administration.

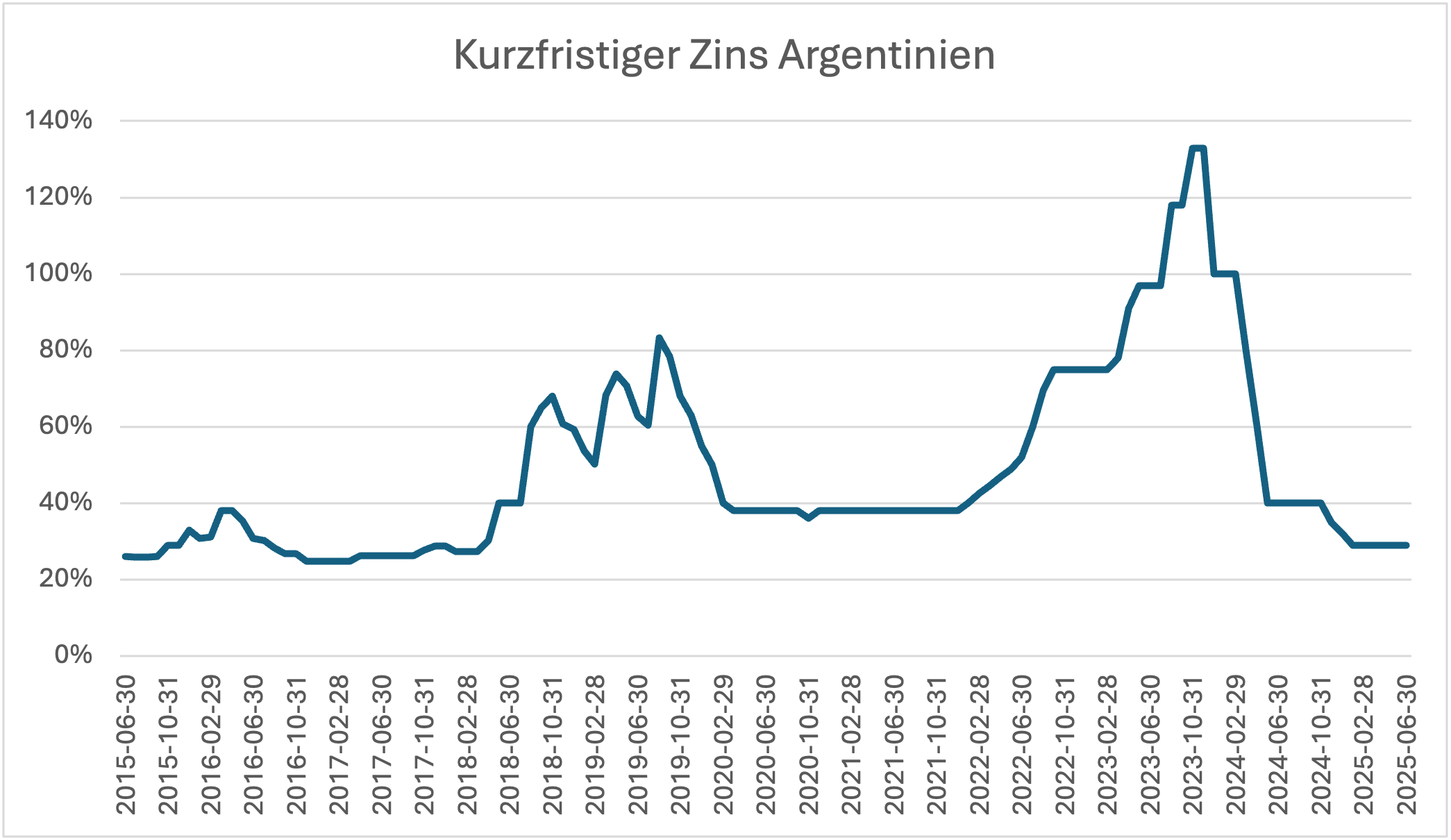

The Argentine dilemma can be seen directly in the interest rate level (Figure 5). Because inflation is still high, the central bank must also keep interest rates high. Currently, short-term interest rates are above 30 per cent. The problem is that no company will take out a loan at such an interest rate and invest without being sure that it can also increase its prices by this percentage in the coming years.

Figure 5

Source: BIS

If the government is determined to further reduce the inflation rate, a potential investor would have to be crazy to take on debt at 30 per cent. Since there is a great deal of uncertainty about the outcome of the entire process, the financial markets do not offer any instruments (such as inflation-indexed loans) that could be used to bridge the disinflation phase. An investment boom by private companies is practically out of the question as a solution to Argentina’s plight.

Argentina is currently grappling once again with the problem that the devaluation could have a lasting impact on the inflation rate. Only if the wage indexation mechanisms are broken in a political process can there be any hope that interest rate conditions will normalise. However, this requires an expansionary fiscal policy aimed at social equality. Only with state protection for the poorest in the population can the trade unions be persuaded to take the risk of reducing the adjustment of wages to the current inflation rate. But that is the last thing one can expect from the libertarian Milei. That is why his failure is inevitable.