Heiner Flassbeck and Patrick Kaczmarczyk

Things have gone quiet around Argentina. The mainstream European press, which euphorically celebrated the president with chainsaws during his election, has largely remained silent two years after that election. Isolated reports of success, such as those published by the Friedrich Naumann Foundation for Freedom in December 2025, have met with comparatively little response. There is a reason for this. There is nothing to celebrate. After two years, it is becoming increasingly clear that the chainsaw has only caused damage and has not improved anything. The libertarian president, who forcibly reduced the government’s current debt to zero and received extra praise from the International Monetary Fund and the economically liberal press in Germany in January 2025, has failed in every respect.

However, interested parties are still arguing against this. They still point to the high GDP growth expected for 2025 by the International Monetary Fund, for example. In December 2025, the Argentine government was still optimistic that growth for the year would exceed 5 per cent, which would have been in line with the estimate made by the OECD last summer. However, surveys conducted by the Argentine central bank already put growth at 4.4 per cent, which is below that figure. More importantly, the hard facts show that economic development in 2025 has not only flattened noticeably, but is also pointing significantly downwards.

In any case, the question remains as to the substance of the figures for 2025, as the previous year’s GDP growth also includes a base effect. Since the Argentine economy slumped massively in 2024, even a slight stabilisation at a low level is enough to suggest high percentage growth. This results in a mathematical increase, but does not reflect a recovery if the hard indicators show no signs of improvement month after month. A look at this data reveals that the signs for the overall economic situation point to stagnation at a low level at best. There are no prospects for a radical improvement.

Real economy in decline

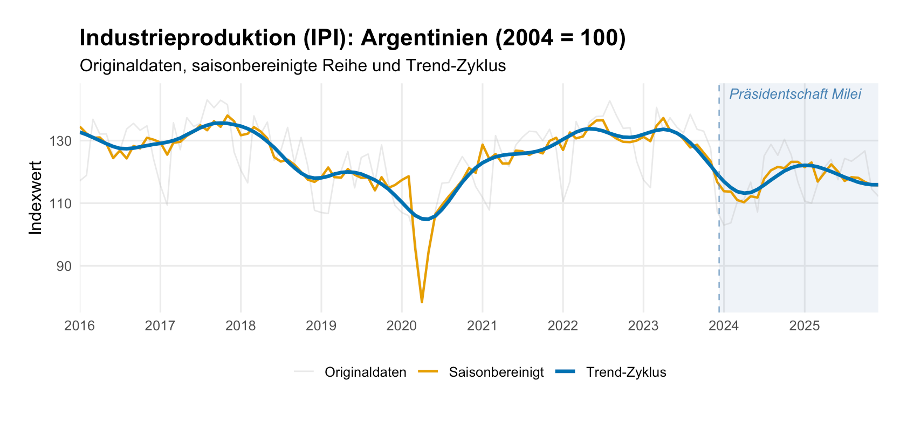

Industrial production is a more reliable seismograph for economic substance than calculated GDP. Since it is based on actual production volumes rather than estimates, it is the hardest indicator of actual economic development. The data paints a bleak picture here: industrial production, which was already under massive pressure before Milei took office, appeared to stabilise briefly in 2024 (Figure 1). However, this effect proved to be temporary. Throughout 2025, the sector returned to a clear recessionary path.

Figure 1

Source: INDEC

The structural crisis is particularly evident in industrial capacity utilisation, which stood at only 53.8 per cent in December 2025 – well below the level of 2023 (65.6 per cent) and also below 2024 (58.1 per cent).

While individual basic industries such as refineries, paper and base metals have recently remained stable or even increased their capacity utilisation, key cyclical sectors are experiencing a massive slump. The automotive industry in particular, with capacity utilisation of only 31.2 per cent, as well as textiles and rubber/plastics, are significantly below the previous year’s levels and far below previous levels. These highly cyclical and employment-relevant industries are particularly sensitive to economic downturns and slumps in demand both domestically and in important export markets.

The fact that the official GDP figures for 2025 show double-digit growth in investment compared to the previous year is again a consequence of figures that only refer to the previous year’s comparison. Gross fixed capital formation, whose growth of over 10 per cent for the whole of 2025 was interpreted in the press as an investment boom, clearly illustrates this: while the year-on-year comparison benefits from the base effect of the massive slump in 2024 (-17.2 per cent!), the quarterly analysis paints an alarming picture: In the third quarter of 2025, investment activity slumped by 6.0 per cent compared with the previous quarter. The contribution of gross capital formation to GDP was effectively negative at -0.1 percentage points in the third quarter.

It is absolutely normal for investment to shrink when industrial capacity utilisation is disastrous. In an environment where every second machine is idle, there is simply no rational basis for capacity expansion. Even in Germany, where industrial capacity utilisation is over 70 per cent, investment is shrinking. An investment-driven upturn is a fantasy of those who refuse to admit that their libertarian hero could fail.

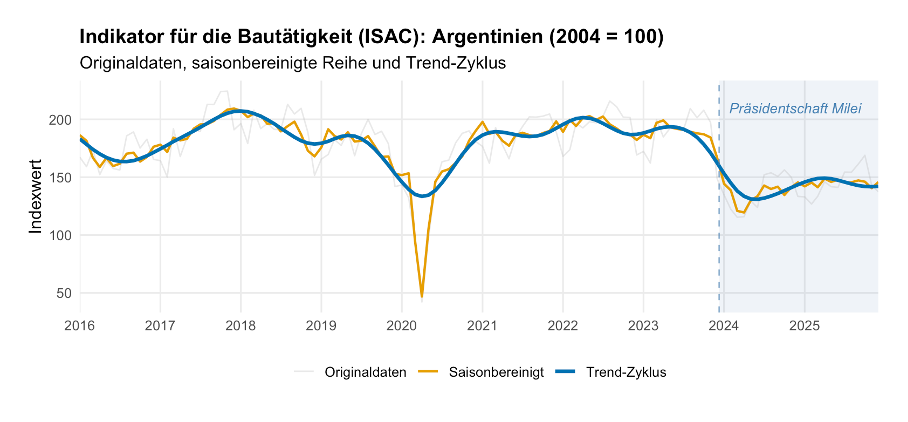

The situation in the construction industry is no different from that in industry (Figure 2). Here, too, the year 2025 has by no means brought the hoped-for turnaround for the better. Although there was a slight recovery after the absolute low point in 2024, there can be no talk of a turnaround or even an upswing. As the figure clearly shows, the fact that the construction industry also recorded a year-on-year increase of 4.4 per cent has nothing to do with an ‘upswing due to bureaucracy reduction’, but rather with the massive slump in the sector in 2024, when there was a 17.5 per cent decline, which in its magnitude resembles a depression. Argentina remains in a deep recession, as can be seen from the course of this curve.

Figure 2

Source: INDEC

The latest available monthly estimates of economic activity (Estimador mensual de actividad económica, EMAE) also give little cause for hope. However, they do show which sectors are driving Argentina’s ‘upswing’ according to the official interpretation. While most economic sectors remain stagnant or are shrinking, the overall index is kept in positive territory by a small group of outliers. These primarily include financial services, with growth of 24.5 per cent, mining, with growth of 8 per cent, agriculture, which is returning to normal after the slumps caused by the drought years of 2022 and 2023, with growth of 6.5 per cent, and hotels and restaurants, which grew by 7.5 per cent.

However, data on the service sector is scarce in all countries around the world.

Overall, the annual average growth rates for Argentina published by some international organisations are a transparent attempt to distract attention from the significant deterioration in the situation over the past year. The IMF in particular seems to be trying hard to defend its euphoric position on Milei’s election instead of giving a neutral and sober assessment. Presumably, political pressure from the US government not to cause trouble for Milei is also extremely high. As far as Argentine GDP indicators are available, it must be noted that the figures for consumption and investment are pure fantasy.

Employment weak, but major ‘reforms’

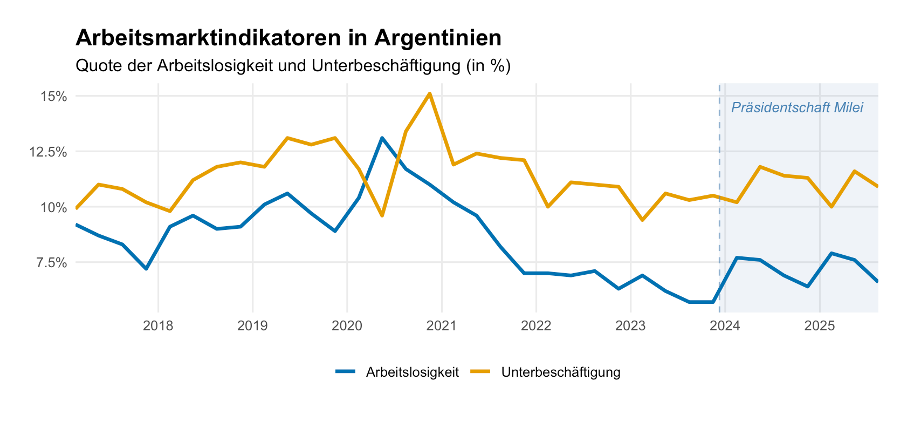

This erosion of the real economic base is still reflected relatively moderately in the employment statistics. However, there is no information on whether and how many Argentinians are no longer registering as unemployed or underemployed. Although the available figures on unemployment and underemployment are still below the record levels seen at the time of the coronavirus shock, at 6.6% and 10.9% respectively, they are higher than before Milei’s election (Figure 3). Here, too, it is obvious that there are no forces that could bring about a change for the better.

Figure 3

Source: INDEC

Now, however, the legal framework is being tightened massively at the expense of employees. A few days ago, the so-called ‘labour modernisation’ passed through Congress – a 100-page reform bill with 218 articles that bears a strong resemblance to what neoliberal economists are calling for in Germany.

What the government is celebrating as a liberating blow against a supposed ‘labour court industry’ is in fact a legal enshrinement of precarious conditions. In future, it will be legal to pay wages not only in pesos, but also in foreign currency or even in the form of benefits in kind such as goods and meals. This marks the return of a form of remuneration that is more reminiscent of the 19th century than of a modern economy. Protection against dismissal is being drastically reduced: in the case of dismissals without cause, the basis for calculating severance pay will be massively reduced, as bonuses and the 13th month’s salary will be ignored in future.

The previous eight-hour model will be replaced by an ‘hour bank’ that allows working days of up to 12 hours without overtime pay. Instead, overtime will simply be offset against future rest periods. Even paid leave will be subject to negotiation in future: Whereas employees previously had the right to at least two consecutive weeks, employers will now be able to divide this time into seven-day blocks. In addition, employees will lose the ability to plan their free time with any certainty, as bosses will now be able to stipulate that holidays may only be taken during the summer months every three years.

This is accompanied by a frontal attack on the trade unions:

In future, companies will be allowed to conduct wage negotiations directly with their workforce, thereby undermining nationwide industry agreements. To ensure that the inevitable protests remain ineffective, the right to strike has been effectively neutralised in large parts of the economy – from logistics to the entire education system – by classifying these sectors as ‘essential’ and requiring a minimum of 75 per cent of staff to remain at work. This has broken the negotiating power of employees – and in a stagnating economy in particular, this precariousness and pressure will have a significant impact on domestic consumption.

Inflation rate remains very high and is even rising

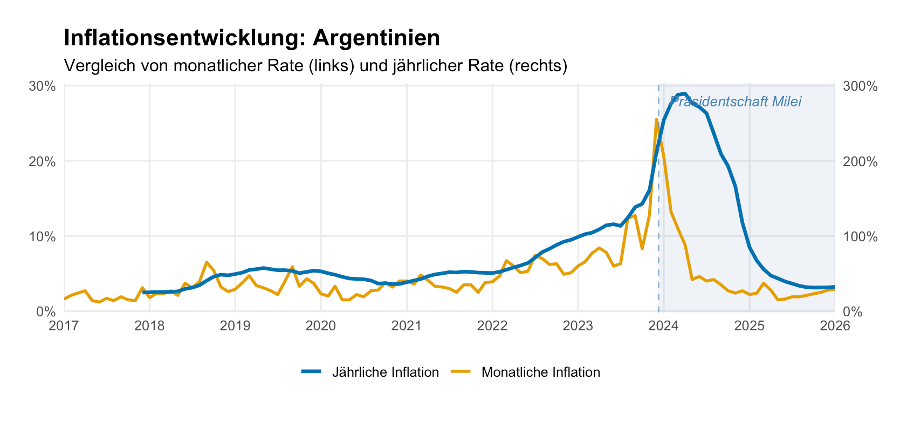

Initial successes in combating inflation are also proving to be unsustainable. In December 2024, the monthly inflation rate (i.e. the month-on-month price increase) was 2.7 per cent. There were then some declines in individual months, but in December 2025 it was back at 2.8 per cent and in January this year at 2.9 per cent (Figure 4). The annual rate is therefore around 32 per cent, with no further downward movement.

Similar to the GDP estimates, however, the inflation figures also raise a number of questions. Just a few weeks ago, on 2 February 2026, Marco Lavagna, the long-standing head of the statistics agency INDEC, unexpectedly resigned from his post. He did not officially give any reasons, but shortly afterwards, Economy Minister Luis Caputo admitted to disagreements about the timing of a planned methodological realignment of inflation calculations.

The price index was supposed to be converted to a modernised basket of goods that better reflects the changing consumption habits of Argentinians (a similar problem can be found in the calculation of the poverty rate in Argentina, which is estimated on the basis of a basket of goods from 2004-2005). The problem for the government was that the new formula would probably have revised the monthly inflation rates upwards. Services, rents and utilities – precisely the areas in which prices exploded under Milei due to the reduction of subsidies – were to be given greater weight in the new index, while food would have been given less weight.

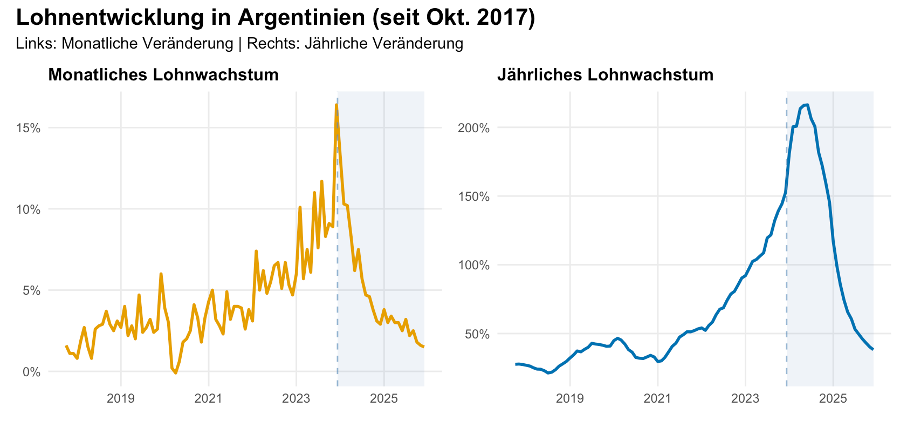

In a remarkable U-turn, the Milei government halted the introduction of the new methodology immediately after Lavagna’s resignation. Caputo justified this by saying that they wanted to avoid ‘speculation about manipulation’ and only implement the change once the process of disinflation was ‘fully consolidated’. The fact that the central bank had already warned of ‘uncertainties’ in the outlook if the new formula produced higher values puts the decision in a different light. However, due to political intervention, the inflation rate remains stuck at just under 3 per cent per month for the time being, while analysts suspect that real inflation has long since picked up again with an honest weighting of rents and electricity prices. The narrative of victory over inflation is thus increasingly proving to be a product of statistical manipulation. Nominal wage growth, which most recently stood at annual growth rates of 40 per cent, also supports this view.

Figure 4

Source: INDEC

The pattern of inflation roughly matches the pattern of wage growth, although overall the growth rates for the latter were significantly lower than for the former (Figure 5). Real wage losses over the past three years are likely to have been significant. It is clear that during Milei’s two years in office, nothing has been done to break the parallelism between wage and price developments through negotiations between the government, trade unions and employers, and to make a fresh start in the fight against inflation. In view of the social tensions exacerbated by the government, this is also unlikely to happen. The belief is apparently that inflation can be brought under control through monetary policy restrictions. This is a serious mistake.

Figure 5

Source: INDEC

Economic policy without a concept

The figures are very incomplete, but there are indications that private households prevented a total collapse of the Argentine economy by reducing their savings (a negative savings rate) after the government had already forcibly reduced its deficit in 2024. As there have been no major changes in the current account balance, this is the only explanation for why the collapse was not even more severe. However, this is certainly not a sustainable solution. If the position of employees is further weakened, it is only a matter of time before domestic demand collapses.

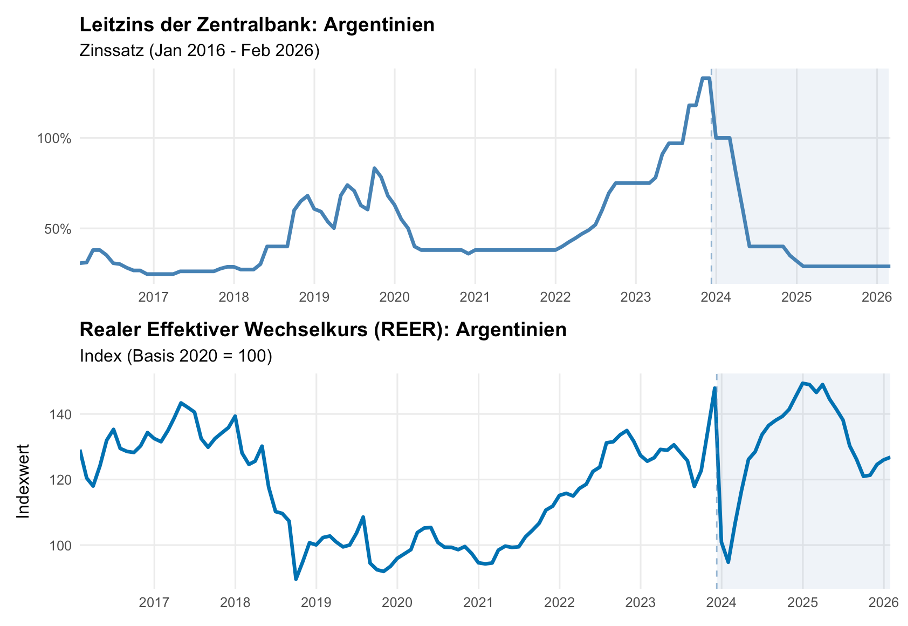

Nothing can be expected from monetary policy either. The interest rate set by the central bank has been at 29 per cent for a year now (Figure 6). For companies, the lending rate is likely to be significantly higher. With inflation at over 30 per cent and the government attempting to significantly reduce the inflation rate, one would have to be crazy to commit to this interest rate level and invest in the longer term.

No relief is to be expected in foreign trade either. Although the real exchange rate has fallen slightly since its all-time high at the beginning of 2025, it is probably still well above the levels at which an external economic recovery could be expected. In September 2025, common estimates put the overvaluation at around 20 per cent. Shortly afterwards, the US government began to intervene massively in the foreign exchange markets in order to alleviate the enormous devaluation pressure. With the rise in the real exchange rate following Milei’s successful election in autumn 2025, Argentina remains uncompetitive internationally.

Figure 6

Source: BIS

Argentina’s balance sheet: the ruins of an ideology

Two years after Javier Milei’s election victory, the Argentine economy is following exactly the path predicted by neutral observers without libertarian blinders. The bare figures belie the ideological optimism of the early days: the real economy remains in deep recession, capacity utilisation continues to fall, unemployment is on the rise and, despite draconian monetary policy, inflation remains at a level that destroys any planning security.

Milei’s unshakeable confidence in his academic guidelines has proven to be a serious mistake. His reference works have lost touch with reality.

This Argentine declaration of insolvency also sheds a revealing light on the current debate in Germany. When parts of the FDP, CDU and AfD, supported by neo- and ordoliberal economists, call for ‘more Milei’, they are in fact advocating a programme of industrial decline. The ‘chainsaw’ does not restructure economies, it amputates the industrial base and stifles domestic demand. Those who praise this course as a model are accepting economic decline in favour of abstract budgetary discipline. Argentina serves as a warning of what happens when economic development becomes a victim of libertarian ideologies. The outlook remains bleak, as Milei’s worldview does not envisage any corrections, even if the ruins in the real economy become impossible to ignore.