Heiner Flassbeck and Erik Münster

In a recent speech, ECB Executive Board member Isabel Schnabel compared the mandates of the European and American central banks and came to the surprising conclusion that the ECB’s singular mandate (namely, to have price stability as its sole objective) is on a par with the Fed’s dual mandate (to pursue employment and price stability as equally important objectives). This very point has been contested on this site on several occasions in the past.

Is a dual mandate unnecessary?

In Schnabel’s view, a dual mandate is unnecessary. She argues that monetary policy measures are very similar regardless of which mandate a central bank follows. She explains this position using the example of the pandemic. She identifies three lessons that must be taken into account.

In the first lesson, she notes that before the coronavirus pandemic, interest rates had been at historically low levels; in other words, there had been a very expansionary monetary policy aimed at stimulating employment and growth. But then came the supply shock caused by the pandemic, which prompted the ECB to raise interest rates sharply. As such shocks could occur more frequently given the current conflicts, she argues that the focus should increasingly be on the inflation target and that the goal of full employment should be regarded as secondary.

That is astonishing logic. A central bank that understands that a supply shock usually triggers a demand shock (as explained here) must focus precisely on full employment, because it knows that the supply shock’s impact on prices is only temporary. Particularly in times of increased supply shocks, a central bank should be able to distinguish between temporary effects on the price level and actual inflation (i.e. an acceleration in the rate of price increases). Consequently, it will not hastily raise interest rates in the event of a supply shock, as this would otherwise exacerbate the subsequent demand shock with its negative effects on employment.

US at full employment, Europe far from it

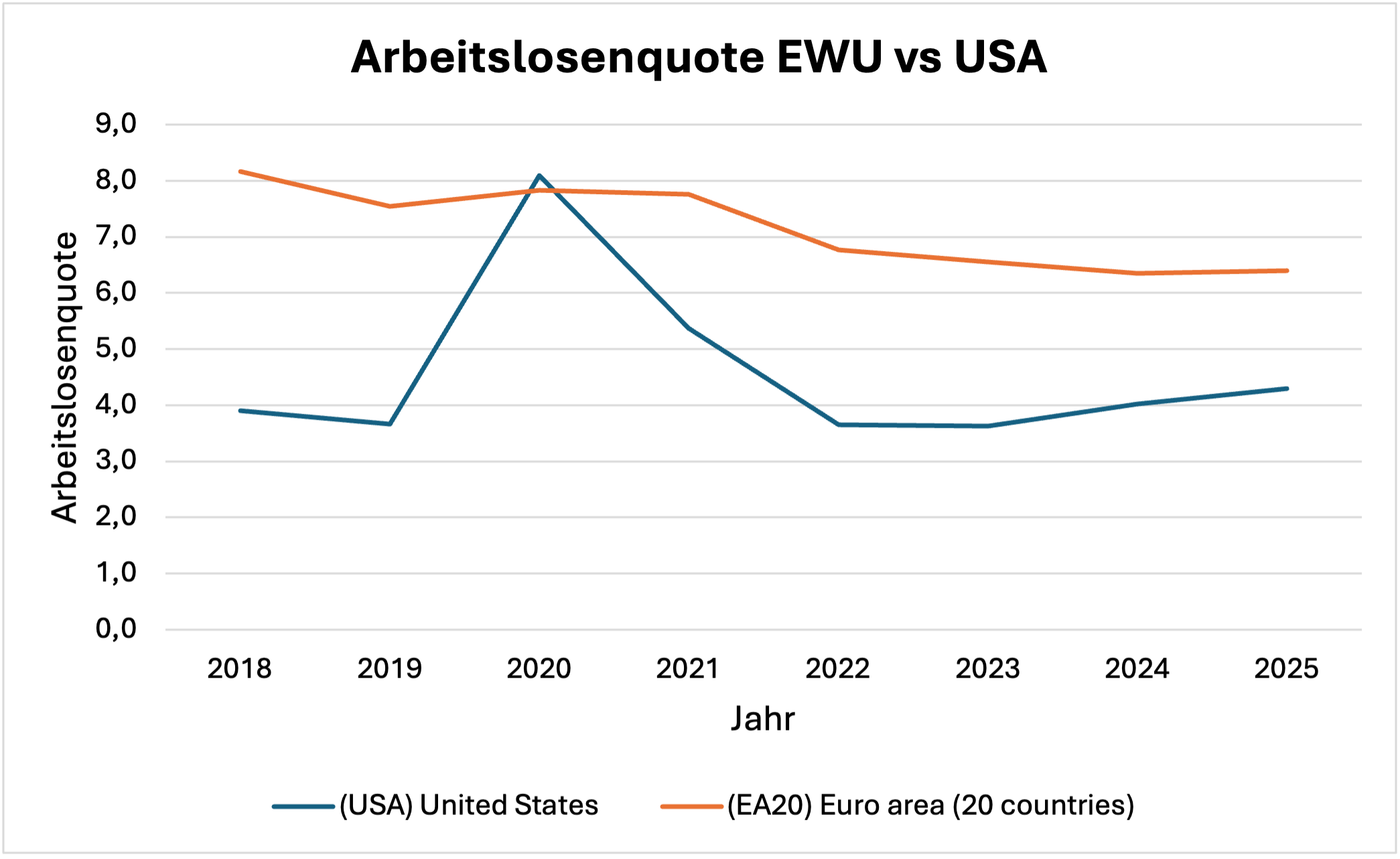

In her second lecture, Schnabel explains why, given the expansionary monetary policy prior to the coronavirus pandemic, it was necessary to focus primarily on price stability in Europe. The overly loose monetary policy before the pandemic had led to high employment levels, which encouraged second-round effects on wages that could then have led to actual inflation. However, the claim of high employment is highly questionable. When comparing Europe with the US, it is downright absurd to speak of a high level of employment in Europe. Figure 1 shows the unemployment rate for the eurozone and the US in a comparison covering the years from 2018 to 2024.

Figure 1

Source: OECD; Unemployment rate US; Eurostat for Europe

Clearly, the labour market in the eurozone – particularly when compared to the US – was anything but ‘tight’. On the contrary, the unemployment rate stood at between seven and eight per cent before the pandemic, compared to four per cent in the US. Although the rate in Europe has fallen slightly since the pandemic, Europe is still miles away from full employment. In the US, the four per cent figure signifies full employment, even when compared to the Bretton Woods era, when the entire world was at full employment.

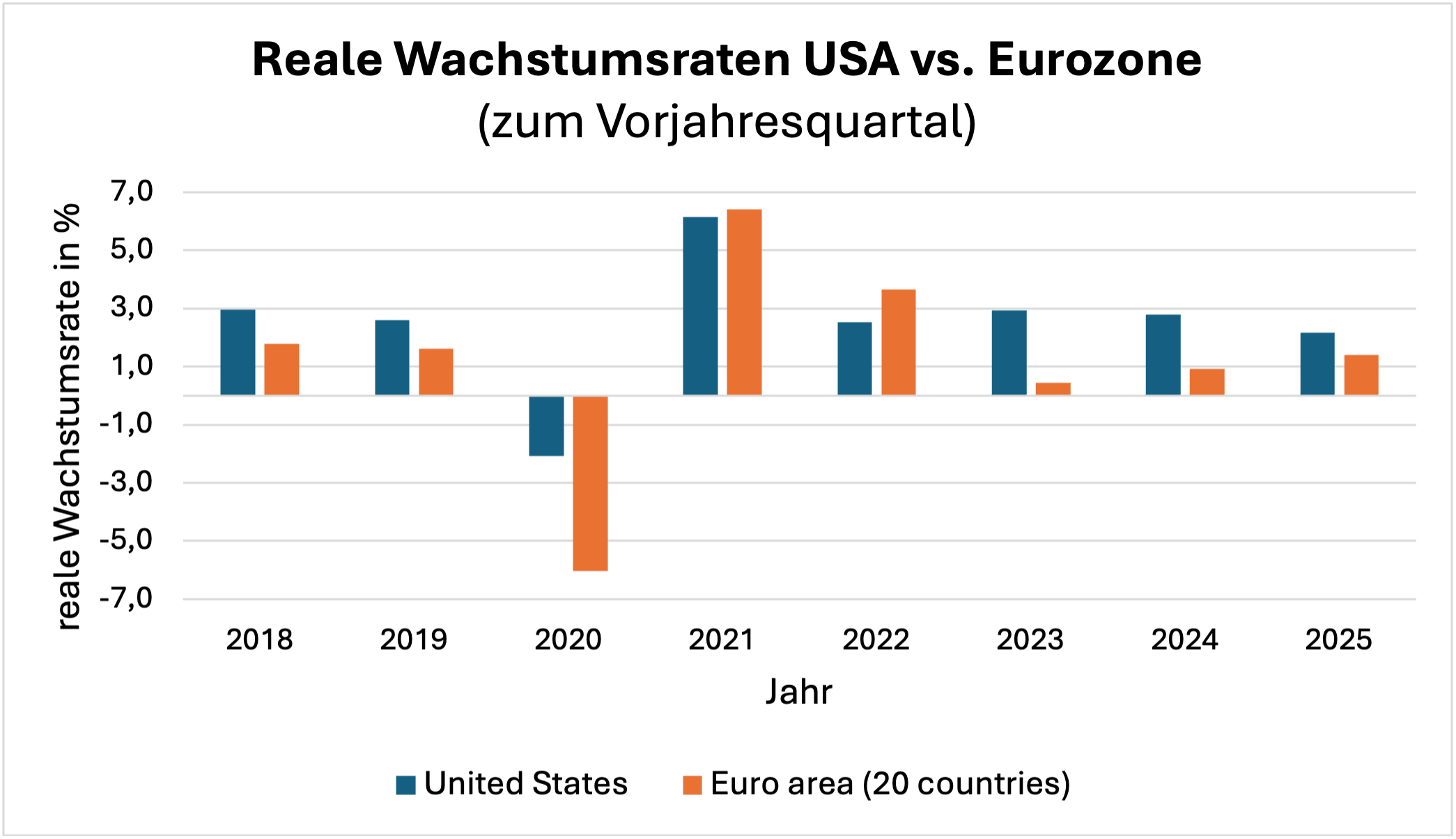

Furthermore, real growth in the US was significantly higher than in the EMU (Figure 2). In particular, in 2023 and 2024, the growth rate in the EMU was below one per cent, whereas in the US it stood at almost three per cent. Consequently, during the critical period following the pandemic, the US had a booming economy close to full employment, whilst the EMU faced an extremely sluggish economy with high unemployment.

Figure 2

Source: OECD

Following Ms Schnabel’s logic, the US and the Fed were far more exposed to the risk of falling into an accelerating inflationary spiral due to second-round effects following the pandemic.

Economic policy in the US far more aggressive in favour of employment

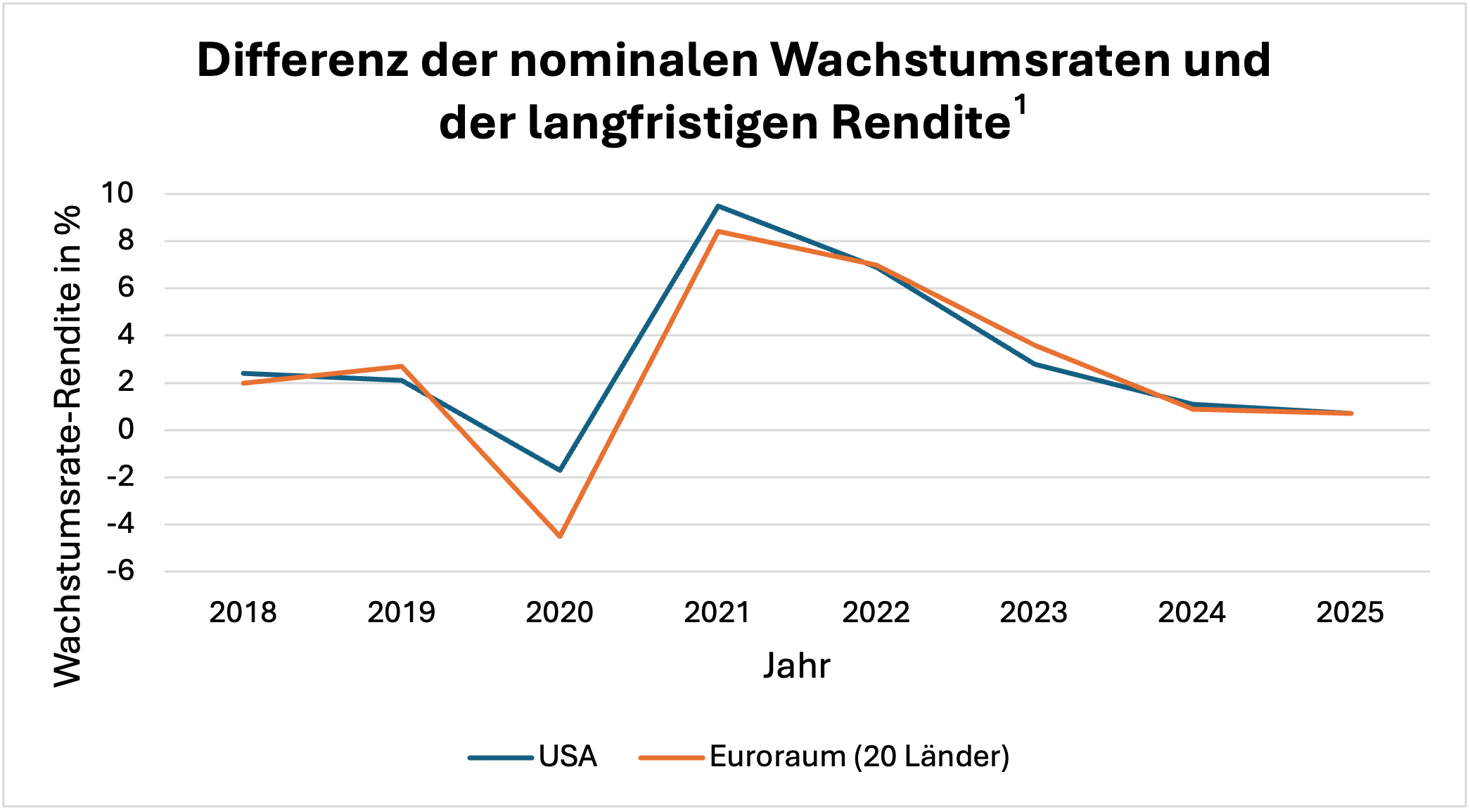

This is also demonstrated by the investment conditions in both regions. Comparing nominal growth and long-term yields (i.e. the yield on 10-year government bonds) provides a good approximation of the answer to the question of whether it is worthwhile to invest more in a country. If growth is consistently higher than the interest rate, it tends to be worthwhile to invest more (Figure 3).

Figure 3

¹Yield on 10-year government bonds

Sources: FRED; Gross Domestic Product, Billions of Dollars, Annual, Not Seasonally Adjusted; Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis, Percent, Annual; ECB, Eurostat; Euro Area 10 Years Government Benchmark Bond – Yield; Gross Domestic Product (GDP) at market prices – annual data

The figures for the period of interest here, from 2022 to 2025, are almost identical. This means that the Fed’s monetary policy was aligned exactly with that of the ECB. However, in the context described above of full employment and high real growth in the US, the impact of US monetary policy must be assessed quite differently from that of the ECB. In the eurozone, either a significant cut in interest rates or an expansionary fiscal policy would have been needed to achieve results as good as those in the US.

European monetary policy was therefore, compared to that of the Fed, anything but expansionary, and everything suggests that there is indeed a significant difference between a central bank having a singular or a dual mandate.

In her third and final lecture, Schnabel continues to champion the cause of liberal supply-side economists. As the European economy is operating close to its potential growth rate, unemployment is low and fiscal policy is expansionary, she argues that a demand-oriented expansionary monetary policy would achieve nothing. If monetary policy is too expansionary, she argues, this could exacerbate a supply shock, much as it did before the coronavirus pandemic. She adds that one must remain vigilant at all times: given the high capacity utilisation in the European economy, the next bout of inflation is imminent. And she said this before oil prices had even risen.

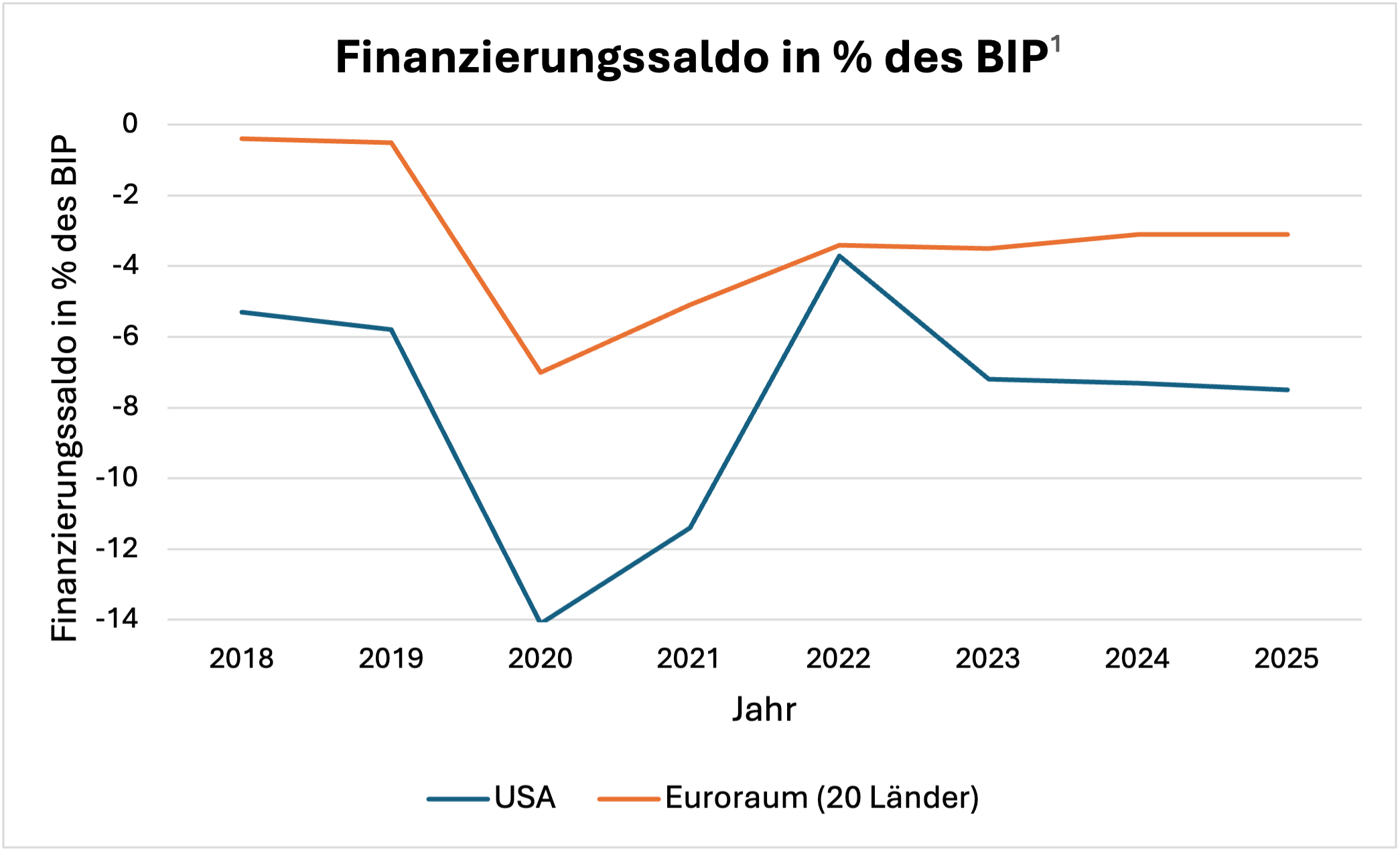

Here, too, one wonders which economy Schnabel is referring to when she says that fiscal policy is expansionary. Europe is extremely far removed from an expansionary fiscal policy. Figure 4 shows the general government net lending for the US and the EMU.

Figure 4.

Sources: FRED; General government net lending/borrowing for the United States, Percent of GDP, Annual. Eurostat; General government deficit (-) and surplus (+) – annual data. For 2025, the OECD forecasts a balance of -7.5% for the US and -3.1% for the euro area)

It is readily apparent that the deficits in the US have been larger than in Europe in every year. This in particular explains why the US consistently achieves far better growth and employment outcomes. In recent years, despite full employment and high growth rates, deficits in the US have continued to rise. In the EMU, they have actually fallen despite very low growth rates.

Conclusion

Ms Schnabel is therefore also off the mark with her assessment here. In Europe, there is neither an expansionary monetary policy nor an expansionary fiscal policy. Demand is too weak and the economy’s capacity is not being fully utilised. Europe is far from full employment. The ECB leadership’s rejection of a dual mandate rests on very shaky ground. One could also view Ms Schnabel’s justifications as a denial of reality.

In Germany and Europe, the economic mainstream has for decades been committed to a division of roles in economic policy whereby the social partners take responsibility for employment and monetary policy takes responsibility for price stability. This is neoclassical economics coupled with monetarism. In a country like the US, where responsibility for employment is directly assigned to monetary policy, there are evidently entirely different conceptions of key macroeconomic relationships. There is no monetarism and no neoclassical labour market where one relies on the assumption that full employment can be achieved at any time through wage cuts.

In Europe, assigning direct responsibility for employment to monetary policy would be interpreted as undermining the responsibility of the social partners and would be flatly rejected by the economic mainstream. In view of this, there is no justification whatsoever for claiming that a dual mandate does not differ significantly from a single mandate. There is a world of difference between the two theoretical concepts and, as shown here, the differences in practice are also enormous. The US performs consistently much better.